International Paper’s John Faraci

When John Faraci, 61, first attempted to climb Alaska’s Mt. Denison, he and his team faced unexpected dangers. A harsh storm set them off course, preventing the climbers from reaching the peak on their first try. During that attempt, grizzlies invaded the camp, consuming much of the food and destroying fuel canisters and the batteries that powered their communication equipment. On the trek down they had to wait seven days for the bush pilots to find them and pick them up.

Similar grit marked Faraci’s transformation of International Paper, which began in 2006, when the company sold its vast forest inventory—“our DNA,” he recalls. International Paper went from being the biggest private landowner in the U.S. to not owning any land at all. (The company did maintain supply agreements on the land it sold.) “We were good, but not good enough to consistently earn the kind of returns our shareowners expect,” Faraci reflects.

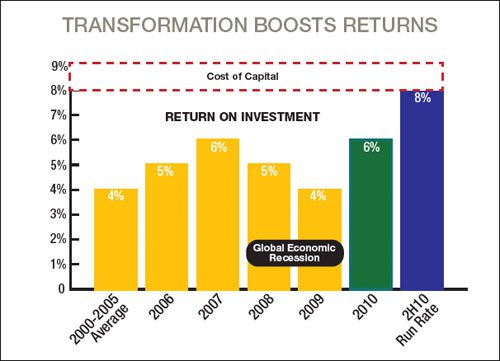

Thinking IP was in too many lines, Faraci sold off a third of its operations to devote itself to its core. Along the way it left its former headquarters in Stamford, Conn., to relocate to Memphis. IP used the $11 billion from the sale of a dozen businesses to pay down a lot of debt, put its balance sheet in better shape and return money to shareowners in the form of a share buyback. It selectively reinvested some of those funds into its paper and packaging business to replace the earnings that it sold. It now owns and operates plants outside the U.S., including Russia, Morocco, Turkey, Eastern Europe and China. The move was completed by 2008—just in time for the economy to hit the skids. The downturn aggravated a long-standing challenge. The industry is highly cyclical and over the last decade rarely earned its cost of capital.

The Summit, N.J.-raised Faraci, who joined the company after graduating from Denison University and notes that his wife “reminds me I’ve been at International Paper longer than I’ve been married,” had come up through finance and served as CFO before becoming CEO in 2003. He shifted priorities to improve free cash flow, manage its supply-demand balance and boost cost-of-capital returns over the industry’s cycle. The $25 billion company with EBITDA of more than $3.3 billion closed 2010 with its best fourth quarter in a decade. The question is, can he continue the momentum or will it prove a peak too far to climb?

Our fundamental strength is our manufacturing capability. We know how to run complicated, capital-intensive factories. If I had to say there’s one thing we do well around the world, it’s our ability to operate these factories and figure out how to improve them every year without spending a lot of capital. But like a lot of industries, there’s no one lever you pull that creates a huge advantage. It’s doing lots of little things well. Execution and experience becomes a competitive advantage.

Transformation Boosts Returns

Our paper business in Brazil is growing four to six percent a year. We’re in Eastern Europe with a large paper packaging operation in Poland, serving the Eastern European market. We have an attractive partnership in the Ilim joint venture in Russia. China is probably our most competitive market. We operate more pulp and paper facilities around the world than anybody else.

The growth in China in some cases can be 15 percent or more. There is a huge amount of capacity, but an equally huge amount of competition. One thing we remind ourselves about China is that fast growth doesn’t mean it’s inherently profitable. It is very competitive.

We do. Our business isn’t a cost-based business; it’s a supply-and-demand-based business. When we think about pricing, yes, it helps when demand is growing. But what really matters is supply-and-demand imbalance. So there are two things that we do: we manage our supply with our demand very carefully, so we don’t build excess inventory and have too much supply.

But we also have a pretty rigorous process for identifying what we call internal margin expansion every year. It’s another way of saying how we improve the cost structure. In slower growth markets you can’t do that by producing more volume. It’s taken a while, but we’ve learned how to do it

well.

Many of our customers sell to consumers. Take the example of a box customer. They’re not going to buy two boxes because we’re advertising them, even if it’s buy one, get one free. They really only need one box to put something in and that’s all they’re going to buy. But, more importantly, we’ve got to differentiate ourselves against our competition by being smarter at figuring out what the customer really needs to be successful. That may mean a new package that uses less fiber. In our paper cup business that makes hot and cold drink cups, we were the first company to come out with a totally compostable, non-petroleum-based coated cup for hot drinks. For companies like Starbucks that have a brand image that’s important to them, having that recycle capability is important. They actually didn’t buy that cup, but because International Paper is viewed as a leader on the environmental front we are partnered with them in other areas.

It’s a pilot program with Starbucks on recycling. We’re the fourth-largest recycling company in terms of collecting recycling material and we’re the largest user of recycled fiber in the country. So we’re at both ends of the spectrum. We’re in the recycling business and we’re also a recycled fiber user. Our industry has a good record of recycling. Most recent data indicates that about 63 percent of the material that could be recycled is. We expect this figure will get closer to 70 percent, which will be good for the environment and great for our customers.

Old corrugated containers (OCC) are compacted by a baler for use in finished products.

Earning our cost of capital has been a challenge for us and for our industry. It’s one of the things that motivated us to transform the company. It’s a cyclical and highly capital-intensive business. In 2010, we met the cost of capital criteria for the first time in probably a decade. Our investors expect us to continue that in 2011. We understand and accept that challenge. The fact that we were able to do so in the second half of 2010 with 75 percent of our company still North American-based is a good sign, but it’s only a sign.

We have real-time transparency in inventory levels. We know what our order book looks like. It’s not a long lead-time business, it’s anywhere from two to four weeks. The industry associations periodically publish aggregate data on supply and demand and operating rates, so you get a window into what’s going on in the broader marketplace.

International Paper is the fourth-largest recycling company in terms of collecting recycling material and the largest user of recycled fiber in the country.

One of the first things I look at most mornings is our safety systems. Because I think one of the most important things in our company is how much progress we’re making to be an accident-free work environment. We’ve improved our safety performance by a factor of 70 percent in 10 years. But we still have too many serious injuries. We’re world-class in our industry, but we now benchmark ourselves against other companies in other industries that are even better than we are.

Safety is a good indicator of product quality, morale, housekeeping and costs. With just about every performance metric you can look it, if the safety is poor, odds are those other things aren’t going to be very good, either.

Having a finance background, you could say I’m a numbers person, but I get most of my information by talking to people. Most of our management team is in Memphis, with the exception of people located around the world, so we all keep each other pretty well-informed, I don’t have to read a bunch of numbers to understand how the business is doing.

0

1:00 - 5:00 pm

2:00 - 5:00 pm

10:30 - 5:00 pm

General’s Retreat at Hermitage Golf Course

Sponsored by UBS