Each New Year finds CEOs seeking smart forecasting that can help guide their business. But while well-paid, future-foretelling outside expert consultants can provide fresh perspectives, there are caveats to taking their authoritative-looking projective graphs too much to heart.

Predictions have long been problematic. John Kenneth Galbraith was one of the most influential economists of the 20th century. Yet, over lunch in 1975, he told me, “The only function of economic forecasting is to make astrology look respectable.”

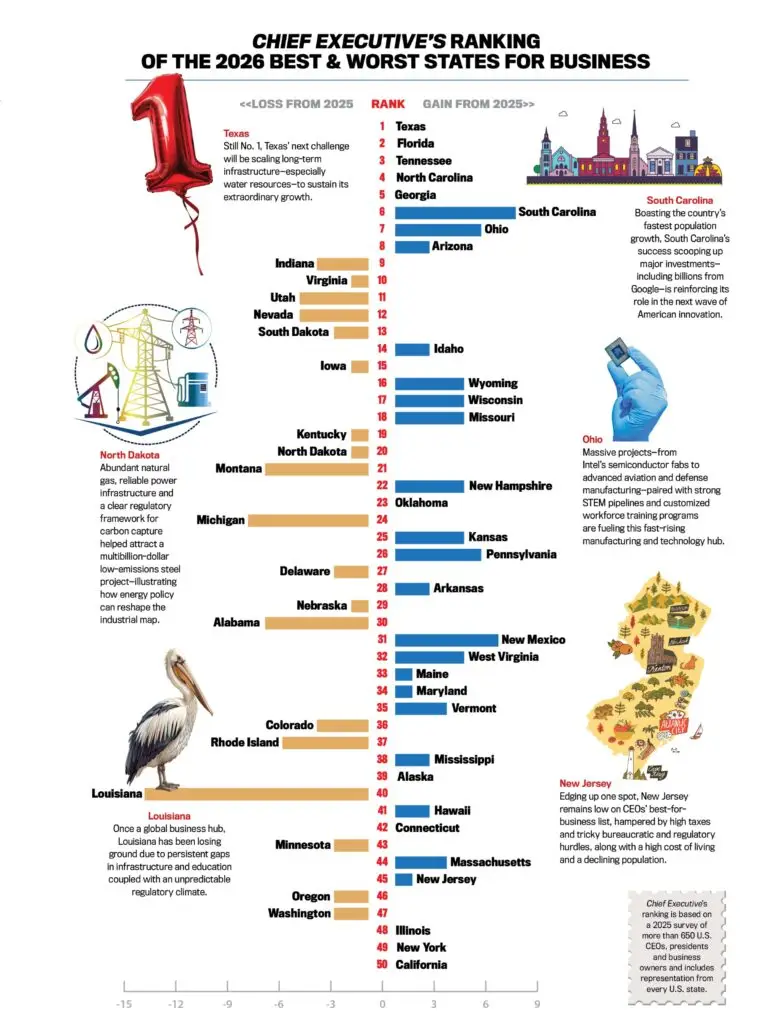

A History of Wrong

Political pollsters widely missed the mark with the midterms—as they have for decades—this time predicting a massive GOP “red wave” that never arrived. The political polling field is draped in seemingly sophisticated data analysis, yet pollsters’ guesses proved no better than your neighbor’s unsupported assumptions.

Business prognosticating fared no better, with bankers and economists flip-flopping over whether the nation was mini recession-bound, about to experience a harsh one, headed for a soft landing or would see no real difference at all. The cynical business pundits decrying a long future of supply-chain jams a year back due to clogged ports and rail lines and trucker shortages disappeared from sight when those problems dissipated in months.

Top Wall Street energy analysts warned of $400 barrel oil prices at the outbreak of the Russian attack on Ukraine, but 10 months later, the prices never approached 25 percent of those estimates. Similarly, energy industry experts warned of President Putin’s redirection of gas exports from the EU to China and India—not realizing that Russia’s gas was in the form of vapor and would have had to travel through pipes that did not yet exist to reach Asia. Royal Dutch Shell, the pioneers of business scenario planning, admitted that they knowingly overstated their own oil and gas reserves by more than 20 percent.

This poor business forecasting has a long history. Journalist-turned-futurist Alvin Toffler’s 1970 business bestseller Future Shock proclaimed that large companies would dissolve into ad-hocracies of nomadic workers rapidly changing occupations in the ’90s. John Naisbett’s 1982 book Megatrends, a New York Times bestseller for two years, completely missed the rise of China and other Asian economies.

Another 1982 business bestseller, In Search of Excellence, made celebrities out of authors Tom Peters and Robert Waterman. Yet, a few years later, more than half the companies celebrated as future winners were underperforming the market. The 2001 original edition of Jim Collins’ bestseller Good to Great showcased a full chapter on Enron’s greatness—the same year it collapsed. Bill Gates’s original edition of his 1995 book, The Road Ahead, failed to foresee ecommerce and the World Wide Web.

The upshot? CEOs should beware of these common forecaster failings:

Straight-line projections: Many “experts” just build off of widely published media reports projecting the past into the future.

Talking their book: Industry analysts are often too close to their clients, selling what they need to please their primary audience.

Biased data sources: Overreliance on phone surveys, nonrandom email polling and pseudoscientific assumptions yield flawed, self-interest-driven projections.

Cynicism and drama sell: Battling for attention in a crowded field, futurists think they fare better and seem smarter the more negative and disruptive they sound.

Lack of candor and contrition: Instead of admitting and learning from mistakes, futurists often cover their trails, seeming to believe that the solution to not being able to predict accurately is to predict often.

As Galbraith cautioned, “There are two kinds of forecasters: Those who don’t know and those who don’t know they don’t know.”