Although interruptions in the global system have often led to nosedives in business sentiment, U.S. manufacturers have paved an unexpected path this month. Confidence is on the rise despite renewed global volatility, on the back of positive improvements in February.

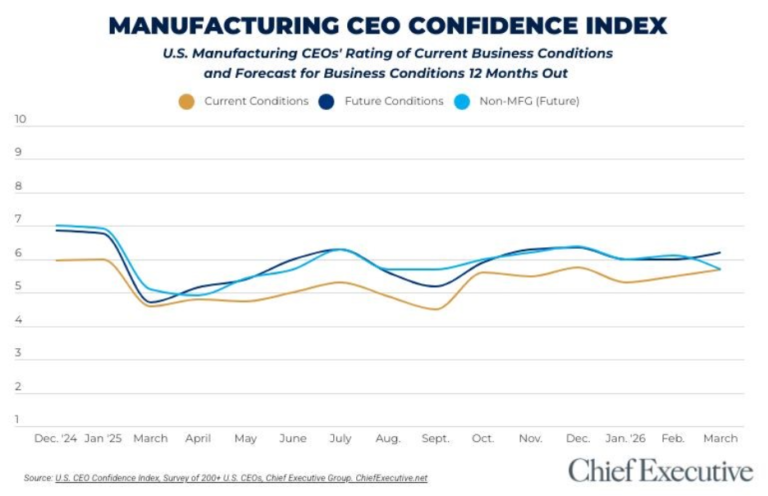

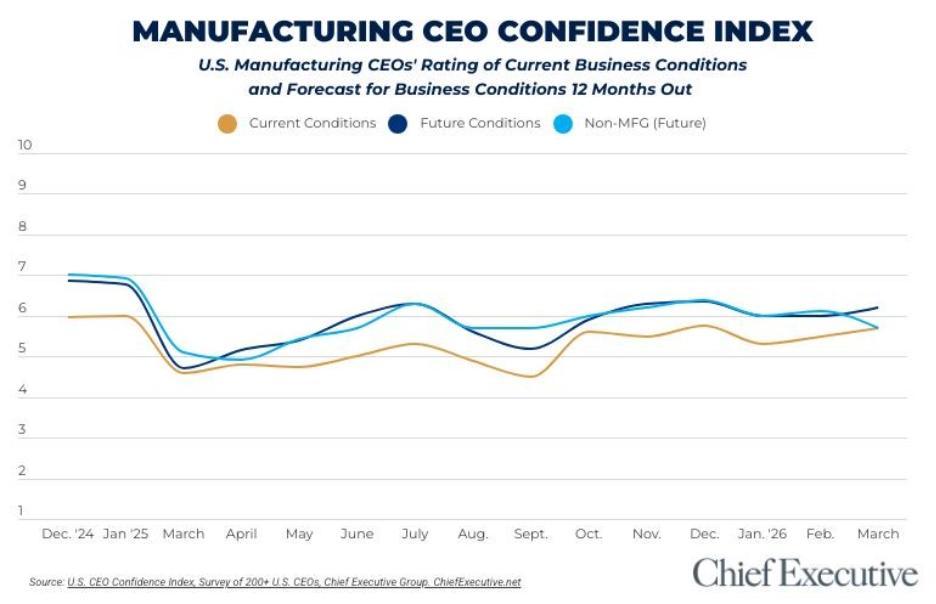

According to Chief Executive’s latest CEO Confidence Index survey, fielded March 3-4 among 237 U.S. CEOs, U.S. manufacturers rate current business conditions a 5.7 out of 10, on a scale where 1 is Poor and 10 is Excellent. This is an increase of nearly 4 percent since February, and it is a perspective both domestic-only firms and those with international exposure share. Non-manufacturing CEOs share a completely different outlook, with confidence cooling in response to volatile pressure.

When asked how that may change in the next 12 months, manufacturers say they expect improved conditions, forecasting business conditions will rise to 6.2 out of 10 by this time next year. This is the most optimistic future forecast provided by manufacturing CEOs so far in 2026 and an increase of 9 percent over current conditions. Non-manufacturers conversely downgrade future forecast, shifting from 6.1 to just 5.7.

Although on face value this may suggest an improvement in sentiment across the board, it has much more to do with the polarization of manufacturers this month than it does with simple change.

Respondents tend to split themselves into one of two groups: the optimists, who are open to adaptability and have experienced healthy real business activity this quarter, and the pessimists, who highlight their concerns regarding renewed domestic and international volatility (especially in Iran) and the impacts that may have on trade and compliance.

Some optimists share that uncertainty has become merely the norm at this point, entrenching itself in the business climate. “People are getting used to the unpredictability of the current administration, but it is becoming the new reality,” said Minnesota-based Jeff Stone, CEO of Navy Island, a family-owned industrial manufacturer with operations across North America, Europe and the Middle East. “Even though interest rates are still likely to stay the same, people have to move on with life and construction will continue.”

Others report bolstered real business activity this quarter, improving sentiment. There is “strength of the order board, backlog and six-month outlook. In addition, inventories are generally in good shape,” says the CEO of a large-sized family-owned manufacturing firm.

What seems to tether the responses of nearly all the optimists was a conviction that volatile dynamics will be resolved, or at least adapted to, by year-end. The CEO of a mid-sized manufacturing firm clarifies this perspective: “Overall demand has been slightly recessionary over the past few years, and I believe these wars and the tariff deals will be resolved a year from now, thus unlocking a lot of pent-up demand.”

Pessimists report almost the inverse of this sentiment and tend to be less future-focused than their optimistic peers. The CEO of a large-sized manufacturing firm notes the “instability and volatility of [this] administration’s policy and now a war in the Middle East” when asked to explain the drivers of his negative forecast, for example.

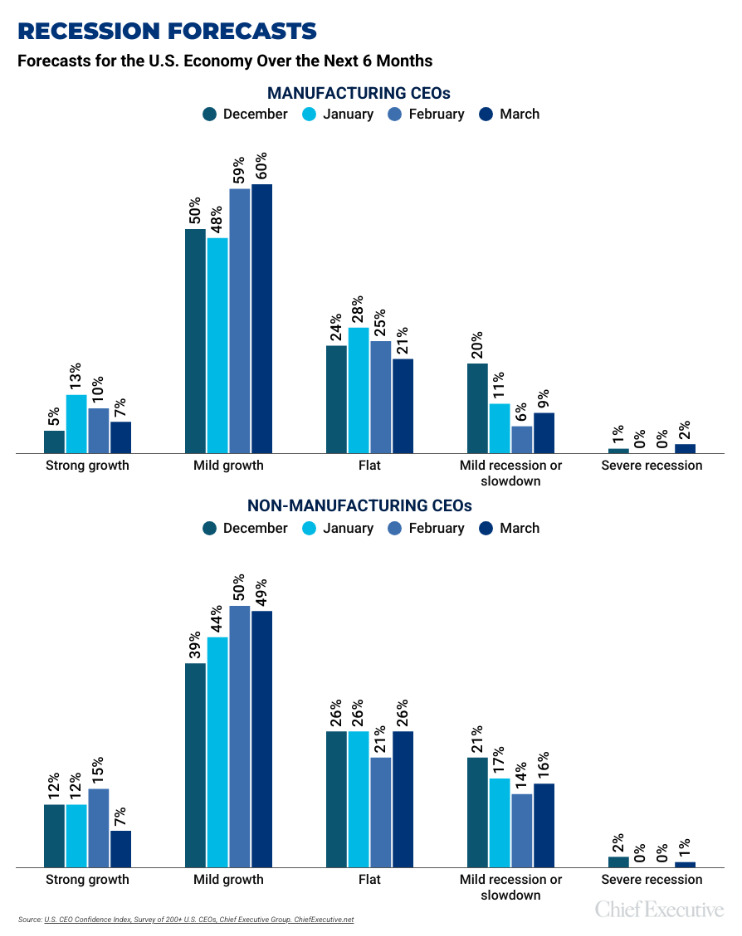

Recession forecasts are worsening mildly this month: Just 67 percent of manufacturers expect to see some kind of economic growth in the next six months, compared to 69 percent in February. Those expecting to see some kind of a recession increased in tandem, from 6 percent in February to 11 percent in March. Manufacturers nonetheless still find themselves well ahead of their non-manufacturing peers, 17 percent of whom expect economic decline by mid-year.

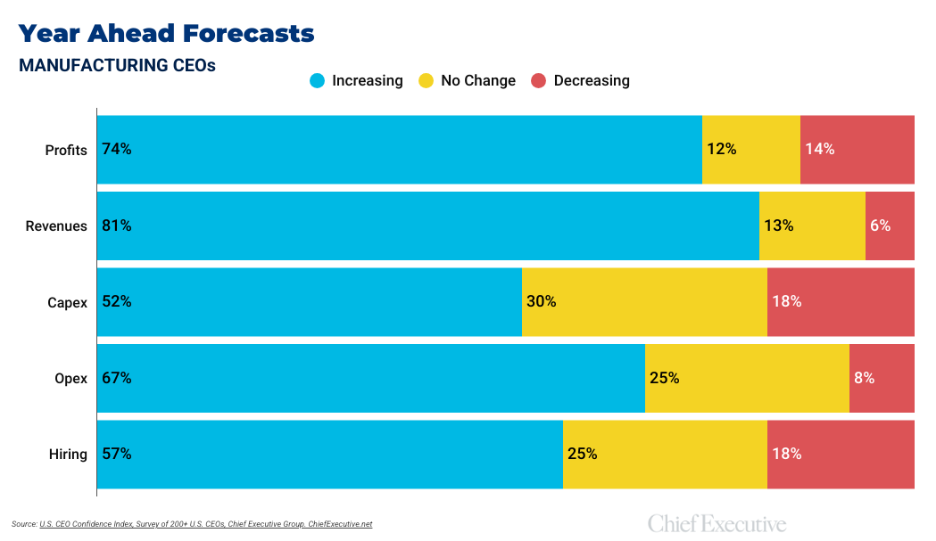

Forecasts for the year ahead vary considerably for this month, reflecting the polarization of the manufacturing sector at large:

- 74 percent of manufacturers forecast profits to increase in 2026 vs. 2025 (down 7 percent since February)

- 81 percent expect revenues to increase this year (down from the 90 percent who did last month)

- 57 percent plan to add to their headcount in the year ahead (up 16 percent from February)

- 52 percent plan to increase their capex this year (down from 56 percent in February)

- 67 percent expect an increase in operational expenditures (down from 68 percent last month)

In terms of capital allocation, manufacturing CEOs are largely focusing on operations, with the top investment area being “operational infrastructure and efficiency,” selected by 44 percent of CEOs. To put it in perspective, the second most popular investment area was “product or service innovation,” selected by only 18 percent of manufacturers.

Another priority present in the March data: hiring. Fifty-seven percent of manufacturing CEOs plan to increase their headcount over the next 12 months, a jump of 16 percent since February and a far higher proportion than the 49 percent of non-manufacturing CEOS who say the same.

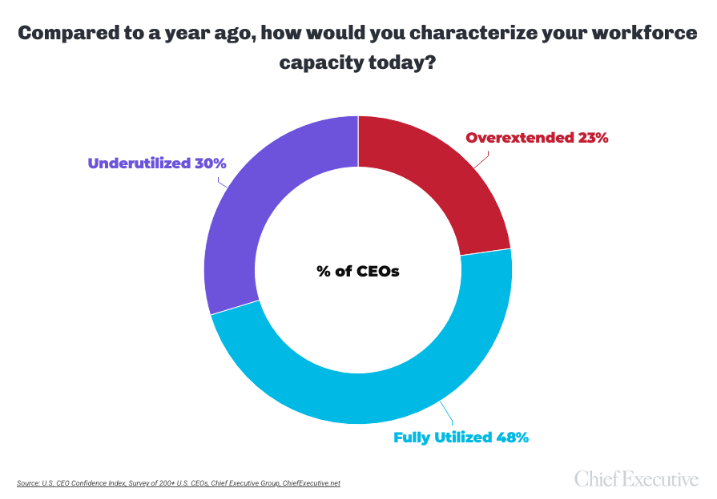

This is again reflected when these CEOs were asked about their workforce capacity, with 71 percent of manufacturing CEOs sharing that it is either overextended or already fully utilized.

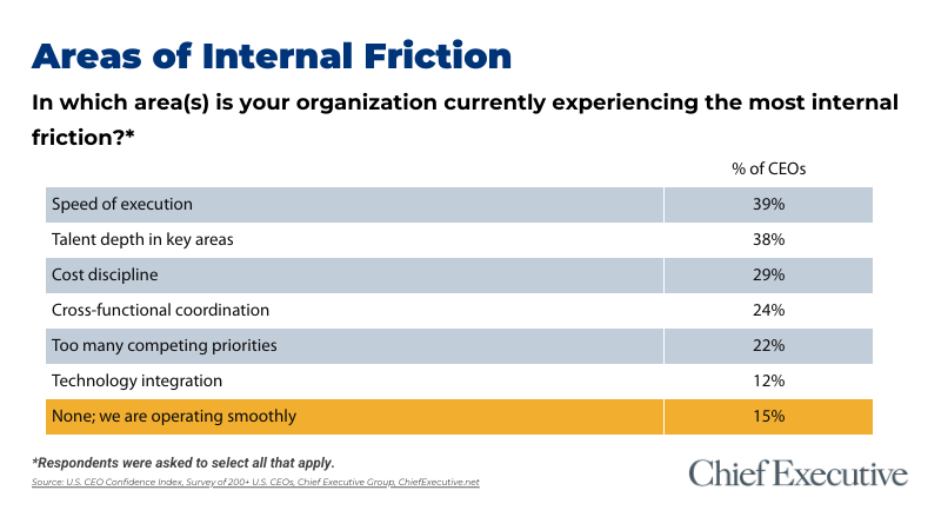

Of course, overutilization can cause internal friction and when asked about it in their organizations, U.S. manufacturers highlight speed of execution as their primary concern. This was closely followed by roadblocks created by talent depth in key areas (the primary concern among non-manufacturers) and cost discipline.

Just 15 percent of manufacturers say that their firms are operating smoothly and without internal friction.