As a result of the executive pay cap in companies taking TARP funding, the door has been opened for increased federal regulation of executive compensation. It is impossible at this point to predict how open the door is and whether or not it is just the first step in an effort by the federal government to control executive compensation in the

This is not the first time that Congress has passed laws that attempt to regulate executive compensation. Indeed, perhaps the most comprehensive effort was the establishment of a wage and price control board during the inflation-ridden 1970s. This effort, like the ones that have followed, is generally considered to have been ineffective. No doubt they changed compensation practices and levels, but not necessarily in the intended way. Indeed, some have argued that past regulation efforts are partially responsible for the high levels of executive compensation that have resulted in today’s demands for controls on executive compensation in the financial services industry and elsewhere.

In 1993, a change in the tax code limited the deductibility of CEO pay as a business expense. It means that corporations can treat only $1 million of salary as a business expense for each of its five top executives. Not covered by this provision are all kinds of incentive compensation (e.g., bonuses and stock). Most agree that the effect of this provision was to establish $1 million as the acceptable level of base salary for top executives. Further, it appears to have stimulated the development of the “pay for performance” plans that have contributed to the high level of executive compensation that exists today.

In 2006, the

Whenever regulations are proposed for executive compensation, the key question is whether they are likely to be effective. In order to answer this question we need to specify what we expect executive compensation to accomplish. Most research on executive compensation suggests that there are four ways an effective executive compensation plan can contribute to organizational effectiveness. It is important to look at each of these and examine whether government regulation of executive compensation is likely to increase the degree to which executive compensation plans support them.

The four are: control the cost of compensation, attract and retain the right executives, motivate the right executive performance and present the right optics concerning executive compensation to key organizational stakeholders. Each of these deserves separate attention, so let’s look at them in turn.

Control the Cost of Executive Compensation

Executive compensation is a business expense, and as such it is appropriate to try to position it at a cost level that is “reasonable” and “competitive.” There is good reason to believe that executive compensation in many

It is highly likely that federal regulation of executive compensation could reduce the total compensation of executives. Regardless of whether new regulations and laws increase the tax rate on high levels of compensation, simply forbid the issuing of paychecks above a certain amount or limit stock grants and stock options, it is likely that government intervention could to some degree reduce the amount of executive total compensation. It is also undoubtedly true that if regulations are put in, a great deal of effort will go into getting around them. Executives in most corporations have extensive corporate resources that they can use to assure that they get the maximum amount of compensation possible, given any regulations that are put in place to reduce their total compensation level. New perquisites are likely to appear, indirect forms of compensation will flourish and executive compensation consultants will have a field day proposing new compensation approaches that will get around whatever regulations or tax provisions are put into place.

At this point, without knowing the specifics of the regulations that might come into place, it is impossible to know what approaches might be used to be sure that executives are highly compensated in the face of restrictions and regulations. Past regulations have led to greater use of stock, deferred compensation, golden parachutes and a host of other compensation programs. Still, it seems likely that the right regulations can lead to some decreases in executive compensation.

Attract and Retain the Right Executives

Perhaps the most important thing that an effective executive compensation plan can do is to attract and retain the right executives. Attraction and retention are influenced by two features of any compensation package: its total amount and what forms of compensation are in it. Obviously, the higher total amount of compensation, the more attractive a compensation package is to an executive. The features of the plan-that is, whether it pays out in stock, cash, short term/long term, etc.-also have a big impact on attraction and retention. Deferred compensation and long-term pay plans can be powerful retention devices, although they may not be highly effective in recruiting senior executives. Stock options, stock grants and bonus plans can be particularly powerful retention devices if the company performs well.

For most companies, the key issue is finding the combination of base pay, incentive pay, stock and deferred compensation that will retain high performing executives. Often, it is not simple to put together a package that appeals to the kind of high-performing executives companies want to employ. It takes a relatively complex mixture of current incentive compensation and long-term incentive compensation. This, in turn, requires cash and stock vehicles that are tied to the individual’s performance as well as the company’s performance. In short, packages often need to be complex and carefully designed. It is because of this that regulations are likely to be very counterproductive when it comes to attracting and retaining the right executives for most companies. They are likely to interfere with creating pay packages that can be fine-tuned and tailored to the attraction and retention needs of particular organizations and individuals. For example, they may make it impossible to pay the kind of attraction and retention bonuses that are needed to get key executives from other firms or to keep them from leaving. They also may make it very difficult to pay the market rate for key executives and to lock them in with deferred compensation.

Pay regulations are likely to be particularly dysfunctional with respect to attraction and retention when only certain industries or parts of industries are regulated. This, of course, is the condition that has been created by the TARP pay cap that was passed by Congress in February. It puts all companies that are subject to the cap at a tremendous competitive disadvantage with respect to attracting and retaining the best executives. They simply cannot compete with private equity companies, foreign companies, etc., for the best talent. As a result, the pay cap legislation is more likely to weaken the companies than to strengthen them at a time when their performance is key to the performance of the

But what about a situation where all

Overall, the correct conclusion with respect to the effect of government regulations on executive compensation when it comes to attracting and retaining the right executives is that it will be more dysfunctional than functional. Perhaps the biggest concern is that it will put those companies that are regulated at a competitive disadvantage to those that are not when it comes to attracting and retaining the best executives. This could be particularly dysfunctional since regulations are likely to focus on the very large publicly traded corporations that are critical to the American economy.

Motivate Performance

Perhaps the most complicated area when it comes to executive compensation is motivation. In some respects, the way compensation affects motivation is relatively simple and straightforward. When all is said and done, individuals tend to be motivated to perform in a particular way when they are rewarded for performing in that way. How motivated they are is very much a function of how clear the connection is between performance and reward, and, of course, how large the reward for performance is. It is this very rationale that has led to large bonus payments for executives and very large stock plans. Incentive pay and stock constitute well over half the compensation of almost all executives today. Indeed, one could argue that many of the problems in the financial industry today are the result of pay plans motivating performance-the wrong kind of performance.

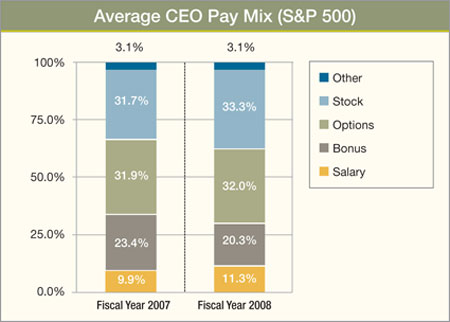

It is almost certain that the motivational power of executive compensation will be dramatically reduced by the pay provisions of any effort to control executive compensation. Not only does the TARP pay cap reduce the total amount of compensation available for incentive pay, it is likely that it will make it difficult to reward the correct behavior. As the many failures of executive compensation plans in the past have proven, it is difficult to get the right performance measures in place when it comes to executives and to be sure that they are paid adequately for the right behaviors. Government regulation is likely to make it more difficult. Indeed, if there are limitations on how much executives can make, it may lead to the unintentional elimination of incentive compensation for executives. Instead of focusing on designing incentive compensation plans, companies are likely to focus on finding ways to maximize executive in bonuses, as profits decreased by a median 5.8 percent. Equilar has its own statistics. Its latest study of S&P 500 CEO pay trends shows that overall compensation levels declined by 6.8% from 2007 to 2008. This is the first significant drop in CEO pay since 2001-2002. Bonuses, which fell by 20.6%, drove the decline in overall compensation. “The drop in compensation demonstrates that in many cases companies do have a true pay-for-performance program,” says Miller. “Specifically, many annual bonuses were hit due to the results for 2008, and maybe more importantly, the value of equity granted in the past has significantly fallen in value along with the stock price.”

With respect to outside directors, 43 companies reduced their pay last year, up from seven in 2007, says Cwirko-Godycki, “marking what may be a trend away from the double-digit board director pay increases recorded in the last several years. “It also appears that board compensation committees are becoming better at doing their jobs. According to a study by DolmatConnell & Partners, an executive compensation firm, the frequency and length of compensation committee meetings are increasing. “Two to three hours has become the norm these days, compared to less than an hour,” says Jack Dolmat-Connell, CEO of the firm.

Compensation committees are evaluating innovative ways to put the brakes on egregious executive pay, without halting corporate growth. One is to examine the amount of accumulated CEO wealth over the long term, via cashed-in stock options, awards and pension credits, before adding to the package with open world and in history. It is possible that by limiting the pay of senior executives, their pay level will become less of an issue with employees, investors and the general public. This, in turn, might make them be seen as more effective leaders and their organizations as being better managed.

There is little doubt that when a CEO’s pay is more in line with that of other employees, it can increase their redibility as a leader and their credibility with investors. This has happened in companies where CEOs have restricted their total compensation to a level which is more in line with that of others in the organization and have been careful to create executive compensation packages that only reward them when the organization’s performance warrants it. It gives them the ability to say they are in the same situation as the rest of the workforce and is often cited as an excellent leadership practice. Although leadership effectiveness is a subtle and hard-to-measure positive outcome of lower and better structured executive compensation plans, it is an important outcome.

Ironically, if regulations are implemented that force lower compensation levels on executives it may do more to subtract from the image of executives who voluntarily take lower and more appropriate compensation packages than it does to improve

the image of others. There is a real danger that they will no longer get credit for having the right executive compensation pay level because in essence they will have to follow the government regulations like everybody else and no longer will be distinctive leaders who make good choices about their compensation.

Further, it is unclear that forcing executives to lower their compensation will give them any additional credibility or lead to their being more positively regarded by the workforce. It may have some effect because it will force them to “live more like the rest of the world,” particularly if they do not have as much access to private jets and other extraordinary perquisites, but they will hardly get credit for the downsizing of their personal compensation if it is mandated by the government.

Overall, there may be more positive than negative effects from the government’s limiting executive compensation when it comes to the public’s regard for executives and, to some degree, for the regard they receive from their employees. A potential negative effect could be the loss of positive regard for those executives who voluntarily downsize their compensation packages. Of course, they can still do this by going beyond the regulations, and undoubtedly some will.

Perhaps the best overall conclusion with respect to the impact, both inside and outside of organizations, of regulations that reduce the total level of executive compensation is to say that they will be on balance positive but not particularly large or significant. Clearly, voluntary reductions on the part of executives would be much better.

The Right Approach

The scorecard with respect to the likely impact of government regulation of executive compensation is not favorable. This raises the question of whether there is a better alternative, and I think there is. Executive compensation is the responsibility of corporate boards; they need to do a better job, but are unlikely to unless governance changes are made. My research shows that 31% of board members feel CEO pay is too high in most cases; another 47% feel it is too high in a few high-profile cases. These feelings are unlikely to lead to action, however, since 85% feel their companies’ CEO pay program is effective. However, there are two key governance changes that might lead to boards creating more effective executive compensation plans.

The first is to require that all boards separate the role of CEO and board chair. This is common in Europe and it may not be accidental that compensation levels are much lower in Europe. In Europe, however, the chair is often a former CEO of the company and cannot be described as an independent chair. In order to have an effective chair, the chair needs to be independent of the company and its executives. This is more likely to lead to a board that makes tough decisions about how

executives are paid.

The second change is putting executive compensation plans to a vote of the shareholders, for whom the CEO and top executives ultimately work. Because shareholders are “the boss,” they are the logical ones to determine CEO compensation.

A first step, which has been taken by less than a dozen major companies, is to make the vote advisory. If this doesn’t constrain CEO compensation, then it is important to move on to a mandatory shareholder vote on all top executive compensation plans.

There are a number of pros and cons associated with shareholder votes, but it is the change most likely to leave companies with the opportunity to design effective compensation plans without government intervention – and at the same time satisfy shareholders with respect to the level of CEO compensation. If it fails to have its intended effect then, and only then, should we consider government-mandated restrictions on executive compensation payments.

One final thought: There is a chance that by moving now to reduce executive compensation levels and improve corporate governance, CEOs and boards can prevent further government regulation of executive compensation.

Edward E. Lawler III is Distinguished Professor of Business at the University of Southern California Marshall School of Business, and founder and director of the University’s Center for Effective Organizations (CEO). Named by BusinessWeek as one of the top six gurus in the field of management, Professor Lawler’s most recent book is Talent: Making People Your Competitive Advantage.