Healthcare costs are crippling American business, and most likely your business. That’s not hyperbole—it’s math.

Since 2001, the average annual premium for family healthcare coverage has gone from roughly $7,100 to nearly $27,000. Single coverage has more than tripled. Starbucks now pays more for healthcare than coffee beans. Auto manufacturers spend more on healthcare than steel.

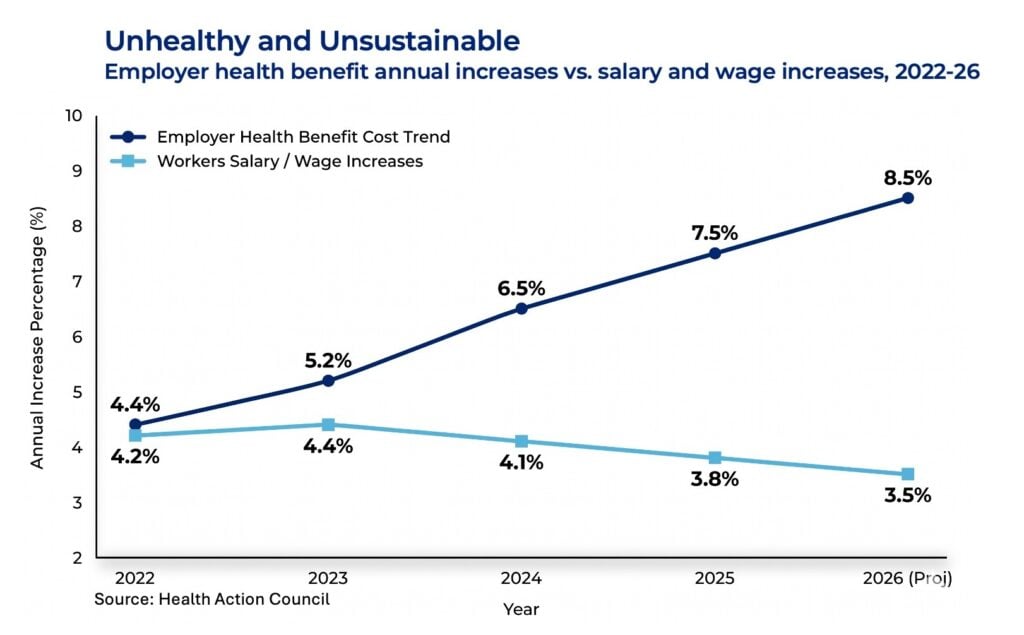

It’s getting worse. Multiple employer surveys and carrier strategy reports put the increase in 2026 healthcare spending at between 8.5 percent and 9.5 percent—the highest in roughly 15 years. The cost of healthcare now affects wage growth, hiring capacity, pricing decisions and, of course, margins. For some companies it affects the ability to invest in growth at all.

Patty Starr has spent years watching this play out—and helping employers fight back. As president and CEO of the Health Action Council, a nonprofit coalition of 240 employers, union groups and nonprofits working to improve employee health and control costs, she’s seen enough to know where the problem actually lives and what to do about it.

“Although we cannot solve this crisis in one year as it’s been building for many,” she says, “we can shift our mindset and manage healthcare costs with business discipline while influencing specific areas of impact.”

In a recent Chief Executive online presentation, she laid out a five-part action plan for employers: practical, do-able steps you can take to rein in your costs and get back some control over what is quickly becoming one of the more menacing line items in your P&L.

The Blind Spot

It starts, she says, by focusing on the right thing. Most organizations spend enormous energy on fixed costs—administrative fees, stop-loss premiums, broker and consultant fees. Those show up cleanly on a spreadsheet. Easy to compare, easy to negotiate and they feel like wins.

The problem, she says, is that they only represent a fraction of most businesses’ total healthcare spending. The real money is in variable costs: claims, service model expenses, network access fees, payment integrity fees, medical rebates, specialty pharmacy. She estimates roughly 75 to 80 percent of healthcare spending is variable. Most organizations barely touch it.

The result: “We win the admin fee spreadsheet,” Starr says, “but we really lose ultimately on our P&L.”

Five Plays to Attack Variable Costs

To start to fix the problem, Starr says you have five control levers that you can access, each addressing a different part of your variable cost spending:

1. Create visibility and control through data.

“You cannot manage what you cannot see or do not know,” Starr says. For self-insured employers, she argues, de-identified claims data should be driving strategy—not arriving as a lagging renewal narrative. Fully insured employers above 100 employees can and should press carriers for meaningful reporting on conditions, utilization, site-of-care patterns and location.

“At a minimum, leaders need medical and pharmacy claims, eligibility and location, high cost claimant details, site of care use, vendor outcomes and employee engagement results. You need enough visibility to ask better questions.” From there, Starr says, healthcare needs to move from an annual review to a quarterly operating conversation. Every quarter, look into: What changed? Why? What action are we taking? Who owns it? How will we know if it worked?

2. Manage the variable cost drivers.

The ER versus urgent care gap tells the story, Starr says. An average ER visit costs about $2,700. Urgent care for the same clinical need runs about $150. Employees end up in the ER not because they’re reckless, but because the plan design doesn’t distinguish between settings and nobody told them otherwise. “Variable cost control means influencing the decision before the claim is created,” she says—through both contract structure and year-round employee education, not a once-a-year open enrollment push.

Geography is part of this too, she says. “Many employers operate as if they have one national population. The reality is you have many local populations. Provider markets make a difference, access differs, social barriers differ. The same diagnostic category can have very different average allowed costs by state and region.”

3. Steer employees to higher-value care.

Not every provider produces the same outcomes at the same cost, and Starr’s point is that a plan treating them all the same gives employees no reason to choose differently. Quality and cost tiering, place-of-service tiering, reference-based pricing, centers of excellence and pre-procedure second opinions can all move the needle—but only if employees know about them.

“Would an employee know the better value choice before a claim?” she asks. “If the answer is no, the plan is relying on people to make sophisticated healthcare purchasing decisions at a moment when they’re either sick, stressed or already confused. Create a structure where the high value clinical choice becomes the easiest path for your employee.”

4. Treat metabolic and chronic health as financial risk.

“Obesity, diabetes, hypertension and high cholesterol—these are real metrics you can measure and drive better outcomes, but they’re also your financial risk indicators.” HAC’s analysis found about 26 percent of member employees were diagnosed with obesity, and that group accounted for roughly 46 percent of total healthcare spend. Adults with obesity ran per-member costs more than twice those without. Men with a metabolic condition were more than seven times as likely to experience a catastrophic event than men without one.

“If the organization waits until a stroke, a cardiac event, kidney complication or a complex diabetes admission occurs, an expensive claim path has already started,” Starr says. “The question to ask is, what are we doing to reduce the probability, severity and repeatability of catastrophic claims where early action can make a difference?”

5. Govern pharmacy like a supply chain.

“Pharmacy has supplier economics, rebates, unit costs, utilization patterns and it also has safety issues,” Starr says. The PBM administrative fee is only the visible piece. The real questions, she argues, are about rebate pass-throughs, spread pricing, specialty drug management, biosimilar adoption, generic-first policies and “polypharmacy.” When employees are on multiple medications from multiple prescribers across multiple conditions, she says, the medication list itself becomes a risk—more side effects, less adherence, more avoidable ER and intensive care utilization.

“The key question is, are we buying the lowest net cost and the safest regimen?” she says. “Pharmacy is too large and too fast moving to be governed only through procurement at contract renewal.”

Governance Is the Multiplier

None of the five plays stick without structure, Starr argues. Without governance, each initiative becomes a one-time HR project that never connects to business outcomes.

In practice, she says, that means a quarterly steering committee with finance, HR, procurement, legal and your broker or consultant, working from an agenda built around population health dashboards, vendor scorecards, member experience and pending decisions. For self-insured employers, there’s also a legal dimension—ERISA requires fiduciaries to act prudently in the interest of plan participants, which means being able to document how decisions were made, how vendors were evaluated and how fees were monitored.

The annual renewal, Starr says, should be the reset of a year of active management. Not the moment strategy begins.

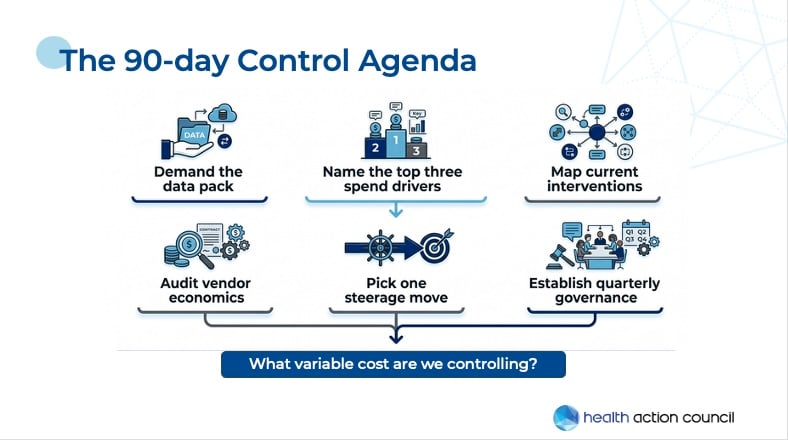

The Next 90 Days

Starr’s biggest piece of advice is that you not wait for renewal season to go after your variable costs. There are things you can do immediately to begin attacking the problem:

- Get the data on your healthcare spending from your broker/provider.

- Name your top three spend drivers.

- Map where you currently have interventions and whether they’re working.

- Audit your vendor economics—how do they make money?

- Pick one move to really steer.

- Establish quarterly governance if you don’t have it.

And always keep the goal in mind: What variable costs are we controlling? It keeps the work from fragmenting into a long list of disconnected benefit projects and forces a connection between action, spend and outcomes.

Do all this, or even part of it, and you’ll have a real shot at bending costs over the next year, she says.

“Employers are not passengers in the healthcare system,” Starr says. “You are purchasers, fiduciaries, workplace strategists and economic actors. Control is about governing a major business expense with discipline.” And it’s very doable.