It’s no longer about rhetoric. It’s now President Obama; Barack Obama the perennial campaigner and gifted rhetorician now has to put the campaign along with the other “childish things” cited in his inauguration speech aside and settle down to governing.

With his party controlling both the House of Representatives and the Senate, Obama’s still likely to get approval for spending a spending stimulus package that will cost $1 trillion or more over two years. If Congress passes such a bill in the coming weeks of about an $800 billion, the 2009 deficit will top $2 trillion. Even the biggest critics of

The CBO shows federal spending in 2009 will be about $3.54 trillion. This number includes the spending effect of TARP and the federal takeover of Fannie and Freddie and are designed to jump-start the economy and create or save 3 million jobs. He plans to speak more about the need to rebuild confidence in a speech on the economy.

This belies a fundamental question: Will it work? But to answer that one needs to understand what it is that makes economies grow in real terms. Successful economic growth has meant that nearly all citizens of the

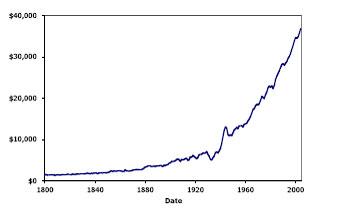

The pace of modern economic growth in the

(In 2004 Dollars)

Source: Louis Johnston and Samuel H. Williamson (2002), “The Annual Real and Nominal GDP for the united states, 1789 – Present.” Economic History Services, September 2004,

Paul Romer the Stanford economic historian and perhaps the best expositor of what makes for real growth explained it this way: “Economic growth occurs whenever people take resources and rearrange them in ways that are more valuable.” It doesn’t get pithier than that.

Romer uses the simple metaphor of the coffee shop to illustrate. “In most coffee shops, you can now use the same size lid for small, medium, and large cups of coffee. That wasn’t true as recently as 1995. That small change in the geometry of the cups means that a coffee shop can serve customers at lower cost. Store owners need to manage the inventory for only one type of lid. Employees can replenish supplies more quickly throughout the day. Customers can get their coffee just a bit faster. Such big discoveries as the transistor, antibiotics, and the electric motor attract most of the attention, but it takes millions of little discoveries like the new design for the cup and lid to double average income in a nation.”

This is where I worry that the Obama brain trust may veer off the track. Do we want our government to be in the business of designing coffee lids? It is not a glib question. Romer’s point is that individuals make the millions of micro decisions every day that amount to macro productivity. If individuals don’t do this or hold back because they are waiting for signals from

Similarly, Keynesian economists believe that government budget deficits “stimulate” the economy during a recession. But we’ve got $1.2 trillion this year and $800 billion next year of deficit “stimulus” without any special “stimulus” package. Isn’t that enough? Going back to Romer’s coffee shop, if one drinks five cups of coffee and that doesn’t stimulate enough, does one drink another five? And five more on top of that? Perhaps it’s time to recognize one’s addiction and start reforming one’s bad habits. Federal policymakers should do the same.

Richard Wagner, a professor of Economics at

Curiously, The New York Times reported that Christina Romer, Obama’s chief economist, “concluded in research she helped write in 1994 that interest-rate policy is the most powerful force in economic recoveries and that fiscal stimulus generally acts too slowly to be of much help in pulling the economy out of recessions.” The problem is that by the time the effects of a stimulus are actually felt it will simply add inflationary pressure to a fledgling recovery, which may have the effect of strangling the recovery baby in its crib.

Last November Wall Street Journal op ed economics editor Stephen Moore spoke to Chief Executive magazine’s annual Leadership Summit about the new administration’s initial 100 days. He presented a graphic reproduced below that underscores the power that tax incentives play in our economy. Basically the higher the marginal tax rate on income the lower the receipts the federal government collects; conversely federal receipts rise when marginal income rates drop. It’s clear that when individuals are allowed to keep more of their income, the more active they become to borrow Romer’s phrase, in rearranging resources into more productive uses.

The key word is productive. This is where business leaders might push forward by making their views known to a newly inaugurated President who is, one hopes, open to listening to ideas that work before the collectivist establishment that controls

The ranking member of the House budget committee, Rep. Paul Ryan (R-Wis.) has come up with a number of promising suggestions that might avoid the policy traps to which our Solons seem drawn. His “Roadmap for

- Provide Help to Those Who Need It. With the economy still shedding jobs, it makes sense to extend unemployment benefits, as we have already done.

- Support Real Policies for Growth. Fast-acting tax policy — such as allowing expensing on all new investments — would boost incentives to expand business operations and create jobs. In addition, lowering the corporate income tax rate — currently the second highest in the industrialized world — would help attract investment in the

- Provide Tax Certainty. In its most recent budget, the Democratic majority assumed the largest tax increase in history by letting a scheduled tax increase in 2010 occur, which would increase taxes on investment, savings, businesses, families and workers. This threat is stifling business investment and job creation today because of the uncertainty in tax laws. Congress should permanently extend the current tax laws and drop tax increases. This would serve as a de facto tax cut, increasing the after-tax rate of return on investment and unlocking billions in private, idle capital.

- Help Stabilize Financial Markets. Existing Securities and Exchange Commission regulations, or the lack thereof, are aggravating the sharp declines in asset values and the confidence in markets. Current mark-to-market accounting rules, last year’s repeal of the uptick rule, and the opaque nature of the credit default swaps market, when combined, are aggravating the distress in our financial markets and our economy. The federal government can help stabilize these markets by reforming the mark-to-market accounting rule to require a rolling average, restoring the uptick rule to put a brake on short selling of stocks to manipulate stock prices, and providing greater transparency in the CDS market.

- Stop Over-Selling What Congress Can Do. Congress must stop pitching the false notion that we can simply spend (then tax and borrow) our way to prosperity. Last year,

- Get Spending Under Control and Address the Long-Term Spending Crisis. Congress must also get control of its own spending — particularly wasteful earmarks, and the unsustainable growth rate of our largest entitlement programs. Our three largest entitlements — Medicare, Medicaid and Social Security — have a current unfunded liability of $34 trillion; and every year we fail to act, we dig ourselves another $2 trillion-$3 trillion in the hole. Without reform, these programs will not only grow themselves right into extinction — they will impose a crushing blow to our budget and economy in the process.