The U.S.-China economic contest has entered a new phase, and every CEO in America is feeling it. Tariff escalations, export controls on critical materials, rare earth restrictions, retaliatory moves—all unfolding at a pace that makes quarterly planning feel like guesswork.

Ram Charan, who has spent six decades advising the world’s largest corporations and their boards, argues that what most leaders still frame as a trade dispute is something far more consequential: a structural, economic war with no end in sight— one in which factories are the front lines, currency is the artillery and your supply chain is the terrain being fought over.

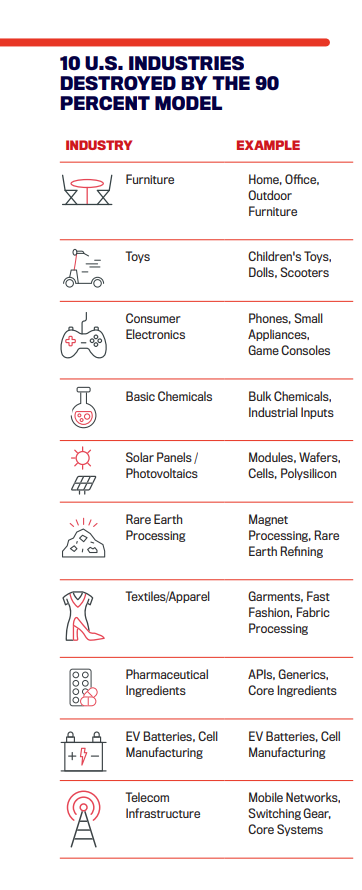

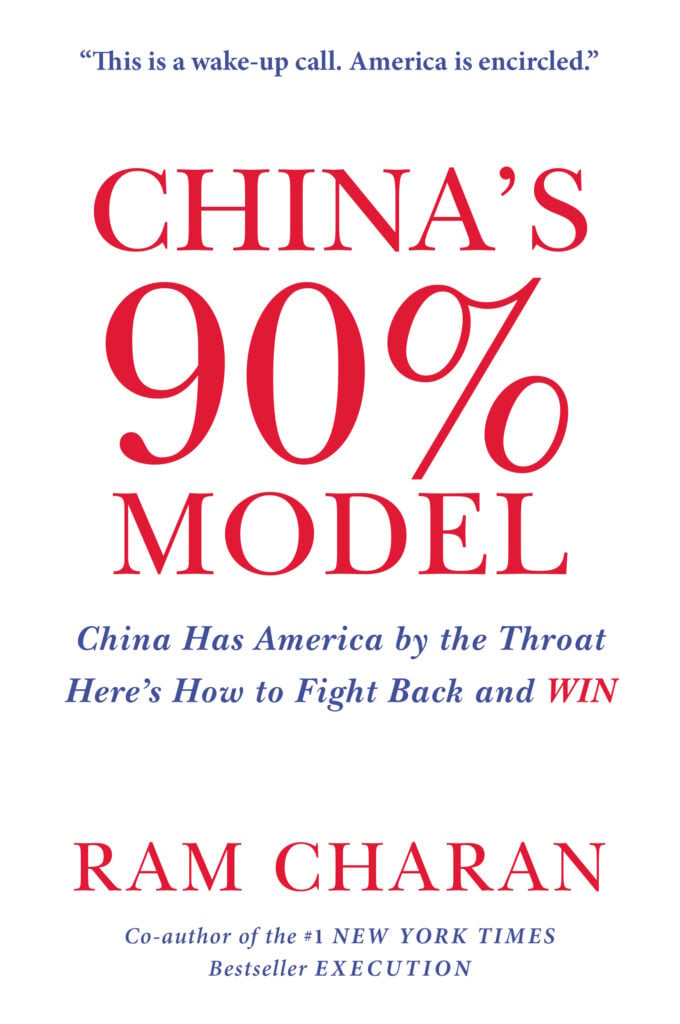

In his new book, China’s 90% Model: China Has America by the Throat. Here’s How to Fight Back and WIN, Charan lays out the full geopolitical case and the coordinated allied response he believes is required to counter what he calls China’s “90 Percent Excess Production Capacity Model,” a strategy designed not merely to outcompete Western industries but to destroy them, sector by sector.

That Great Game of global dominance, of course, is far beyond your control. The chapter we excerpt here is aimed squarely at the CEO and the boardroom, at controlling what you can control. It’s an operational playbook for leaders looking to avoid becoming victims as the world’s two largest and most interwoven economies deepen their conflict, a guide to some of the most essential, even existential business questions of our time: how to extricate from China, where to find growth on the other side and how to manage the pain of transition without losing your investors, your credibility or your nerve.

Charan—who has advised more than 200 companies and roughly 100 boards, including more than 30 years of work inside China—beaks it down industry by industry: chemicals, semiconductors, pharmaceuticals, critical minerals, automobiles, telecom. He maps a three-to-five-year timeline. He names the hard questions you need to be asking now. And he is characteristically blunt about the costs, arguing that short-term margin pressure is the price of long-term strategic control. “This is not a recession path,” he writes. “It is a transformation path. And the companies that move first will define the next era.” Here is an excerpt from his book, edited for clarity and length. — Dan Bigman, editor

Convergence means one thing: becoming one focused unit against a destructive opponent. In China’s 90% Model: China Has America by the Throat. Here’s How to Fight Back and WIN, I lay out the playbook— how governments should coordinate, what machinery they must build and what support businesses will need.

But here is the reality: governments create the conditions, the support, the incentives, the framework that enables businesses to operate in new ways. But governments cannot rebuild industries themselves. They cannot relocate supply chains. They cannot protect technology or innovate at scale.

Only you can do that.

You are on the front line of this economic war. Every decision you make—where to invest, where to source, which markets to prioritize—affects not just your company’s future, but the outcome of the broader contest. You have contributed to China’s rise, often without realizing it. Now you can help break its march. This is your playbook. Step by step. Industry by industry. How to extricate from China, where to find growth, what skills and equipment you need, and how to navigate the pain without letting it become a recession. Because this is not a recession path. It is a transformation path. And the companies that move first will define the next era.

Why Now?

The window for controlled strategic withdrawal is narrowing. The national shift is already underway. President Trump has made reducing the trade deficit with China a core priority. Every month that passes, tariffs rise, supply chains shift, technology controls harden and China tightens retaliation. Delay will only make the eventual exit more painful, and less on your terms. Washington and Beijing are moving. But what matters more is what you do.

If you sit on a board, or lead a company, ask yourself five questions:

1. Do you have a focused strategy that excludes China?

2. Are you transparent about your presence there?

3. Have you built a transition plan that’s executable now?

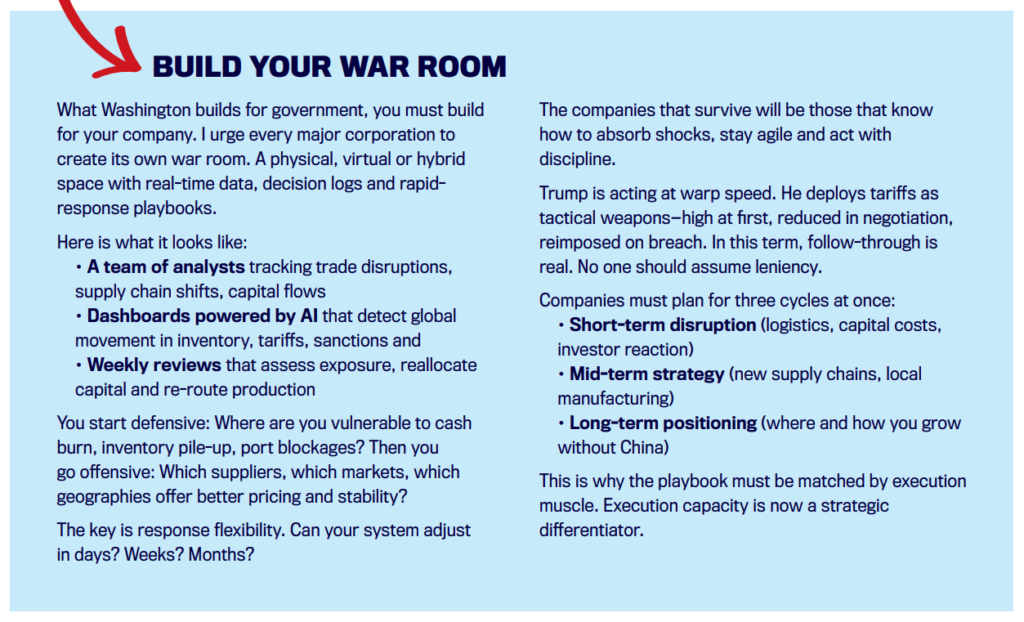

4. Do you have a war room tracking early warning signals of adverse changes ahead?

5. Are you communicating with the board and investors with the quality and frequency this moment demands?

If not, you are vulnerable. China will keep inviting companies. They will offer facilities, even subsidies. But only while you are useful. And if your product has military or industrial application, that use is short-lived. Once they get what they want, they will cut you off. That is the playbook.

It has happened before. It will happen again. Ask Tesla. Ask Micron. Ask GE. The choice is no longer whether to act. It is when and how. Later in this article, I will show you the warning signs and how to determine your timing.

Finding Growth Beyond China

Extricating from China is only half the battle. Once you step out, you must know where and how to step in. Start now. Do this in parallel. Companies that wait to extricate before finding growth will shrink into defensive shells. Companies that move decisively can seize new frontiers of growth. Two pillars define this future: the Global South and the American Sphere.

Beyond these lie 180 unaligned countries with $25 trillion in GDP. Most will choose the American Sphere over China’s model. Together, they offer the markets, the talent and the stability to counter China’s assault and build a stronger foundation for the next era.

Global South: The Next Frontier

In my 2013 book Global Tilt, I wrote that the action would shift below the 34th parallel. Today, that future is here. From Latin America to Africa to Southeast Asia, these economies hold the people, infrastructure needs and hunger for technology that define the next wave of opportunity.

The numbers tell the story. South Asia is the world’s fastest-growing region, expanding at nearly 6 percent annually. India alone is growing between 6.5 and 7 percent—the fastest among the world’s largest economies. By 2028, India is expected to overtake Germany to become the world’s third-largest economy. By 2030, its GDP is forecast to reach around $7.3 trillion.

At the same time India is becoming a major global manufacturing and export hub. Apple now produces over $10 billion worth of iPhones in India annually. EV firms are looking to India as a global base. Companies that build in India are not just serving India, they are serving the world. But India is not alone. Vietnam’s economy is expanding at more than 6 percent, Indonesia at about 5 percent. Nigeria, Kenya and Ethiopia are emerging as Africa’s new industrial anchors. Brazil and Mexico remain Latin America’s manufacturing powerhouses. The global pattern is clear: Growth and competitive industry are becoming widely distributed across the Global South.

Large economies across the Global South will tilt toward the American Sphere. China’s debt traps, seized ports and crushed local industries are creating backlash from Sri Lanka to Zambia to Pakistan. Democracies want to trade with democracies—without the strings attached. The opportunity is mutual: Trade with the American Sphere brings new standards of living and positive trade balances.

But it will not be business as usual. These are not plug-and-play markets. Managers must unlearn what worked in China. Here is what will be required:

- Capital and staying power. These economies do not yet offer deep local funding. You must bring the capital and know-how.

- Different scale logic. Many markets are smaller. You may need to build regionally—India serving as a hub for multiple geographies.

- Tailored innovation. Use AI and local data to adapt products to new needs. Smaller batch sizes. Local assembly.

- Hands-on leadership. You cannot delegate these moves. New org structures, business models, local networks, government relations—they all matter.

Done right, the Global South offers not just risk mitigation, but real growth.

American Sphere: A Stable Base

Alongside the search for new markets, companies need a stable base to anchor their expansion. This is where the American Sphere comes in. It is an industrial platform, a network of trusted economies where manufacturing and advanced industrial capacity can be rebuilt at scale. The American Sphere’s $60 trillion economy, growing at 3 percent annually with stable currencies, represents $2 trillion in new market opportunity every year.

For companies exiting China, this sphere provides what no single market can offer: secure supply chains, predictable rules and co-investment opportunities. It is the foundation on which bets on the Global South can be made with confidence. A protected base where innovation and production can flourish without CCP interference.

The six powers—the U.S., the EU, Japan, South Korea, Israel and the UK—offer complementary strengths: American innovation and capital markets, European industrial depth, Japanese precision manufacturing, Korean electronics and battery technology, Israeli cybersecurity and defense technology and British financial infrastructure.

And critically, as my book outlines, the convergence framework can provide the umbrella you need: tax incentives, low-cost loans, price protection mechanisms and regulatory relief.

The Extrication Process: Industry by Industry

Let me make this concrete. I recently worked with a company that manufactures cellphones and laptops. They came to me asking: How do we reduce dependence on China?

We broke it down. Component by component. What do they need to make? What skills, equipment and materials are required? What do they have? What do they need to get? Where can they get it? Here is what we discovered:

What they had:

- Design capability and brand

- Distribution networks

- Customer relationships

- Capital to invest

What they needed:

- Manufacturing capacity outside China

- Supply chain for critical components (processors, displays, batteries, casings)

- Skilled workforce to operate the lines

- Equipment and tooling

Where they could get it:

- Equipment: Japan, Germany and the U.S. all produce precision manufacturing tools.

- Materials: Diversify sourcing across American Sphere (Taiwan for chips, South Korea for displays, the U.S. for software).

- Skills: Bring in Chinese experts on one-year contracts to train local workers, then phase them out.

- Capital: Leverage convergence framework—tax incentives, low-cost loans, regulatory fast-tracking.

The plan:

- Year 1: Build pilot line in India or Mexico with transferred Chinese expertise.

- Year 2: Scale production, train local workforce and diversify component sourcing.

- Year 3: Phase out China dependency entirely, establish regional hubs. The conclusion? It can be done. Not overnight. Not without investment. But the path exists. This is the model for every industry. Break it down. Component by component. Skill by skill. Then build it back, smarter and more resilient.

What This Could Look Like Across Industries

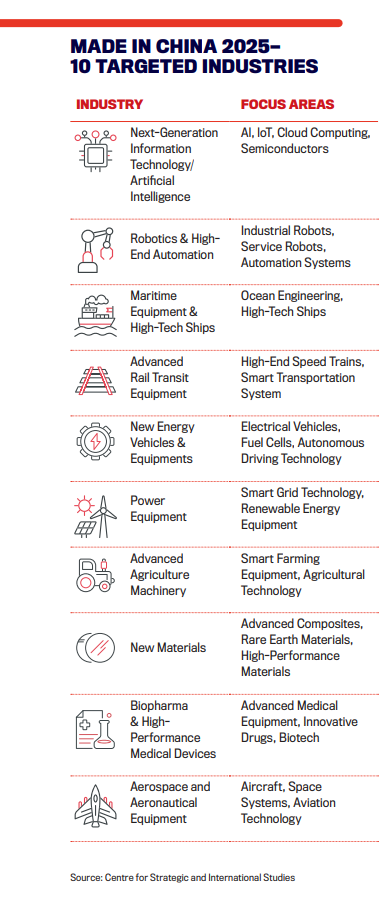

In the book, we identify that convergence must address the 10 made-in-China-2025 industries plus sectors critical to national security, defense and raw materials. The same extrication principles apply across all of them. Here we show how it works through six industries that span the full range:

Chemicals:

- We have specialty chemical R&D and advanced formulation capabilities.

- What we need: Restore domestic production of base chemicals and polymers gutted by the 90 Percent Model, while expanding capacity in the advanced specialty chemicals (catalysts, precision additives and high-purity compounds) that China’s processing operations require.

- Where to get it (examples): Build facilities in the U.S. and Germany, leverage existing European chemical infrastructure; partner with Japan on precision materials.

Critical Minerals:

- We have mining resources (U.S., Canada, Australia) and processing knowledge.

- What we need: Refining facilities, separation tech, magnet production capacity.

- Where to get it (examples): MP Materials expanding in the U.S., Lynas in Australia/Malaysia, Israel for precision extraction technologies, coordinate across American Sphere for full supply chain.

Pharmaceuticals:

- We have the R&D and formulation knowledge.

- What we need: API production capacity, fermentation facilities, quality control systems.

- Where to get it (examples): Build facilities in the U.S. and India, partner with European chemical suppliers, leverage Israeli biotech innovation.

Semiconductors:

- We have design capability (the U.S. dominates chip design).

- What we need: fabrication plants, advanced lithography equipment, supply chain coordination.

- Where to get it (examples): TSMC building five U.S. plants, ASML for equipment, Israel for chip design and cybersecurity integration, coordination across American Sphere.

Automobiles/EVs:

- We have brand, design and assembly knowledge.

- What we need: Battery supply chain, electric drivetrains, charging infrastructure.

- Where to get it (examples): Build battery plants in the U.S./ Europe, partner with Japan/South Korea on components.

Telecom:

- We have network design and equipment manufacturers (Ericsson, Nokia).

- What we need: 5G infrastructure buildout, trusted supply chains, cybersecurity integration.

- Where to get it (examples): Partner with European equipment makers, leverage American software capabilities, Israeli cybersecurity integration, coordinate standards across American Sphere.

The pattern is consistent: We have more than we think. What we need is coordination, capital and the will to build.

Show the World We’re Catching Up

One critical element: demonstrating progress. You do not need to achieve full self-sufficiency overnight. What matters is showing visible momentum.

Set clear milestones:

- Year 1: Pilot production/proof of concept

- Year 2: 25 percent reduction in China dependence

- Year 3: 50 percent reduction

- Years 4-5: Full diversification

When investors, governments and allies see tangible progress—factories opening, jobs created, supply chains functioning—confidence builds. And confidence accelerates investment, which accelerates progress. This is not about perfection. It is about trajectory. Show you are moving in the right direction, and the ecosystem will support you.

What you need to succeed

When you plan, be brutally honest about what it takes:

SKILLS:

• Bring in experts, even from China, on limited contracts to train your workforce.

• Invest in technical training programs with partners across the American Sphere: Japan for precision manufacturing, Germany for machine tools, the U.S. for automation and AI, Israel for cybersecurity and defense applications, the UK for industrial design.

• Build institutional knowledge that stays with your company.

EQUIPMENT:

• Source from trusted partners: Germany for machine tools, Japan for precision equipment, the U.S. for software and automation.

• Negotiate as part of the convergence framework (when available) for better pricing and financing.

MATERIALS:

• Diversify sourcing across the American Sphere.

• Build relationships with alternative suppliers now, before you need them.

• Participate in critical minerals initiatives.

CAPITAL:

• Leverage the Treasury and Commerce umbrella (when available): tax incentives, low-cost loans, price protection.

• Use convergence support (when available) to offset transition costs.

• Model the investment over three to five years, not quarterly.

TIMELINE:

• Year 1: Stop new investment in China, build pilot capacity elsewhere.

• Years 2-3: Scale production, diversify supply chain, train workforce.

• Years 4-5: Complete transition, achieve independence.

PAIN POINTS (BE HONEST):

• Short-term margin pressure.

• Higher input costs during transition.

• Potential Chinese retaliation (price wars, market access restrictions). • Investor anxiety and stock volatility.

BUT THIS IS NOT A RECESSION:

This is an investment in resilience. Companies that complete the transition will have:

• Lower geopolitical risk,

• More control over their destiny,

• Access to growing markets (Global South, American Sphere),

• Government support through convergence framework, and

• Long-term competitive advantage. One company, critical to China’s goals, ran a 10-year scenario model. They are now exiting in five. Quietly. Safely. On their terms.

Breaking the Chokeholds

Diversification into new markets is not enough if China still controls the chokepoints of global industry. Even as companies relocate production and rebuild supply chains, Beijing’s grip on critical materials, technologies and processing systems remains formidable. These chokeholds, from rare earths to battery components, are leverage points China can weaponize at any time. Breaking them is a strategic imperative.

The challenge is not just mining or access. It is conversion: turning raw minerals into usable industrial inputs at scale. Today, much of this processing capacity sits in China. Yet China’s processing depends on American Sphere inputs it cannot replicate, creating mutual leverage, as the previous chapter detailed. Building alternative processing capacity in the American Sphere will demand coordinated investment, new infrastructure and updated ESG frameworks. The cost is high. The cost of inaction is higher.

Recent moves show what is possible when urgency meets execution:

• MP Materials and Lynas are expanding rare earth refining and magnet production in the U.S., Australia and Malaysia to cut dependence on Chinese intermediaries. MP’s billion-dollar Texas facility, backed by the Pentagon, will scale output from 1,000 to 10,000 metric tons, supply Apple and GM and anchor a full domestic supply chain from its California mine to high-grade magnets for EVs, defense and clean energy.

• Trump’s Defense Production Act order is accelerating U.S. mining. In March 2025, the Defense Production Act was invoked to fast-track permitting and funding of critical mineral projects for national security.

• Ukraine has opened its vast critical minerals reserves to the U.S. The U.S. now has access to Ukraine’s significant deposits of lithium, titanium and other essential minerals, valued in the trillions.

• General Motors and Redwood Materials are building a large-scale battery recycling and cathode production facility in Nevada. The project aims to close the loop on EV supply chains and sharply cut reliance on Chinese battery inputs. These are early moves, but they set the tone. Breaking the chokeholds will require scale, speed and coordination— not just nationally, but across the American Sphere. Without it, companies will remain exposed to the very vulnerabilities they are trying to escape.

And here is where your role matters: demand that your suppliers diversify. Audit your exposure. Build redundancy into critical inputs. Use the convergence umbrella to fund alternative sources. This is not optional. It is survival.

The Boardroom Reckoning

Let me give you one final lens. I have sat in boardrooms. I have seen the shift. One $5 billion company wanted to invest $75 million in China with a state partner. On paper, a solid return. But a director asked the right question: “Are you creating your own executioner?” The project was shelved.

Another, a $10 billion firm, wanted to dominate solar in China. But the board asked: “Are we competing with companies, or with a nation?” Again, no-go. This is what real leadership looks like. Ask the hard questions. Revisit the assumptions. Plan for a new future.

Seek Truth from Those Inside

Speak to CEOs who have tried to leave or are in the process. They will not speak publicly, but they will tell you privately what really happens when China decides you have outlived your usefulness. Ask them:

- When did pricing pressure start?

- When did profitability begin to erode?

- When did the CCP demand more data, training or tech disclosure?

- When did subsidies stop, replaced by forced capital injections just to survive?

Use their timeline to predict yours. The pattern is consistent. And it is accelerating. What used to take five years now happens in three. If others in your industry faced pressure in year four, you will face it in year three. Plan your exit before the pressure starts.

These stories are real, even if few are told publicly. European governments are already tracking them. Washington should do the same. The transparency will help boards and journalists understand what is really happening. Because this trend is accelerating.

Ask Yourself the Hard Questions

If any of these answers are yes, then the decision has already been made. You are being squeezed out. Your market share is falling. Their capacity is rising. And if their capacity exceeds local demand, you are under the thumb of the 90 Percent Model.

Act with Credibility, or Don’t Act

Your investors may not like the message. Your board may push back. The analysts may downgrade your stock. That is fine. But your credibility must stay intact. Say what you mean. And deliver what you say. I have worked with CEOs who have done this right. They faced investor anxiety head-on. They explained the plan. They gave specific downside guidance. They framed the transition as a necessary sacrifice. And when the short-term pain came, they did not blink.

Yes, the stock fell. Yes, some shareholders ran. But those who stayed were the right ones. And post-transition, the business came back stronger. Strategic control returned. And credibility, the rarest currency in leadership, stayed intact. That is the bar now.

Prepare to Lose Investors

Do not soften the message. Do not hedge. Do not delay. Tell the truth early. Lay out the path. Show investors what to expect. Not just the dip, but the destination. Let the fast-money crowd rotate out. What matters is who stays, whether your team believes, and most of all whether you execute and follow through.

Build your post-China strategy with specifics: fund it, set milestones and stick to them. Because the next board meeting, the next investor call, the next town hall—they will all ask the same question: What is the plan? You cannot afford to bluff.

The Leadership Moment

The hardest decisions are the ones no one else can make for you. Every board, every CEO, now stands at that edge. The choice is not whether to stay in China a little longer or leave quietly someday. The choice is whether to lead when it matters most.

The companies that will define the next era are those whose leaders face the pain upfront and move with discipline. They will take hits. They will lose investors who were never truly aligned. But they will emerge with control over their future. This is not a recession path. It is a transformation path. The convergence framework (when executed) will provide the umbrella. The American Sphere can provide the foundation. The Global South provides the growth. And you provide the execution.

The window for hesitation is closing. But the window for opportunity is opening. The companies that move first— with clarity, capital and courage—will not just survive this era. They will lead it.

You have the playbook. You have the support. You have the markets. Now execute.

From China’s 90% Model: China Has America by the Throat. Here’s How to Fight Back and WIN (Ideapress Publishing, March, 2026), Copyright 2026 Ram Charan. Excerpted with permission of the author, and available now at major retailers.