The share of U.S. CEOs expecting business conditions to improve over the next 12 months slipped to 48 percent in May, from 52 percent in April, as the war in Iran, rising costs and policy uncertainty pushed more chief executives into a “wait-and-see” stance. Yet overall sentiment barely budged; it stalled rather than soured.

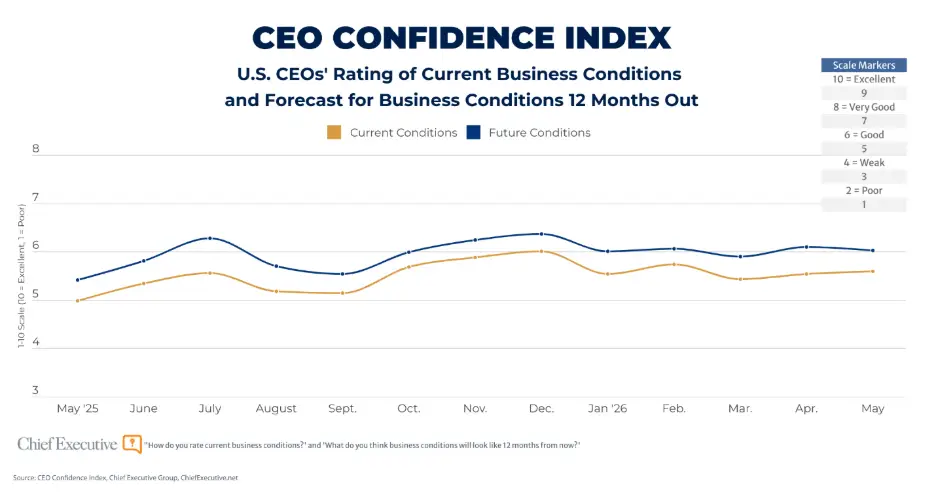

Chief Executive’s May CEO Confidence Index, based on responses from nearly 350 U.S. CEOs polled May 5-6, shows their perception of current business conditions little changed from April. CEOs rated current conditions 5.6 out of 10, versus 5.5 last month and the second-highest reading of 2026 so far, behind February’s 5.7.

CEOs’ 12-month outlook held steady as well, at 6.0 out of 10 versus 6.1 in April—an expected 8 percent improvement by this time next year. The forward-looking component of the Index has hovered at that level since the start of the year.

Some CEOs describe that expectation as partly aspirational. “It’s human nature,” explained the CEO of a family-owned business in the healthcare space. “We like to anticipate change for the better.”

The drivers of sentiment remain unchanged from recent months as well: geopolitics, costs, demand and policy. But May’s data shows those forces aren’t pushing all CEOs in the same direction.

Geopolitics was cited by 57 percent of CEOs who expect conditions to worsen, but also by 43 percent of those who expect conditions to improve. Among pessimists, the concern is often tied to tariffs, supply-chain pressure, energy costs and weaker demand. Among optimists, it shows up as a source of relief.

As one CEO noted: “Iran conflict resolution within 3 months reducing oil prices and continued consumer confidence.” Another pointed to “Geopolitics calming down, return of consumer confidence.”

The outlook for inflation shows a similar split. 46 percent of pessimistic CEOs cited costs or inflation as factors in their forecast, but so did 38 percent of optimists. For some, costs are weighing on demand. “Uncertainty of future costs is influencing demand,” said one CEO. Others expect relief: “Gas prices will come down, which will lead to overall costs coming down,” another wrote.

Demand is also a key driver of CEOs outlook this month. Thirty-eight percent of optimistic CEOs cited demand, customers, market activity, orders, backlog, projects or growth opportunities for their upbeat views. The CEO of a large construction firm forecasts business conditions a year out at 8 out of 10—well above the average—citing “strong new project orders, growing backlog and increasing opportunities.”

“Increased quote activity, booked results YTD up over last year, so far able to recover cost increases,” said another CEO. “More PO’s are starting to come in and more RFQ’s are coming in as well. The market is just cautious now,” added another.

And while fewer CEOs are betting on a stronger year ahead, they are not turning sharply negative either. Twenty-three percent expect conditions to worsen, nearly unchanged from last month. The difference showed up in the middle: 30 percent now expect conditions to remain flat, up from 26 percent in April.

That tracks with the comments CEOs shared throughout the poll: business hasn’t stopped, but limited visibility makes it nearly impossible to forecast in either direction.

“A non-stop stream of events standing in the way of leaders making long term decisions,” said the CEO of a mid-sized professional services firm.

“Strong backlog presently, and opportunities are still strong,” added the CEO of an upper-middle-market firm, but “Uncertainty in the world creates a less optimistic look for the next year.”

Economic Forecasts

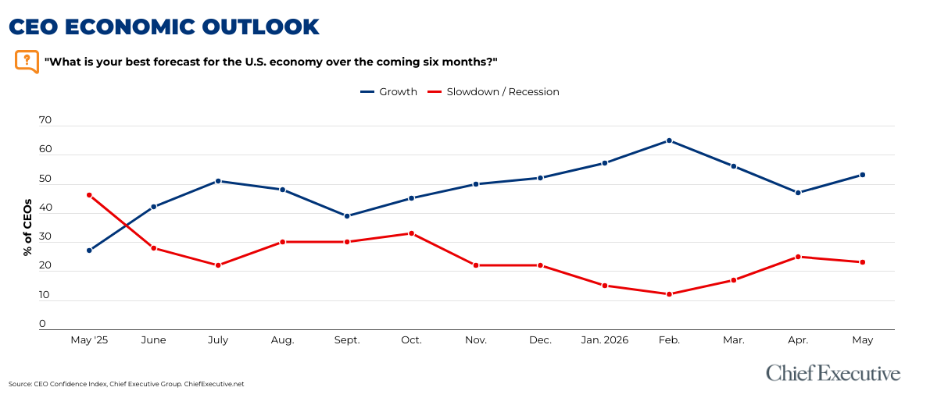

Recession forecasts eased in May after spiking in April to a six-month high. A slim majority of CEOs—53 percent—now expect economic growth in the months ahead, well below February’s recent peak of 65 percent before the war in Iran.

Inflation expectations also eased. CEOs now forecast an average 12-month Headline Consumer Price Index rate of 3.6 percent, down from 4.6 percent in April and back in line with the 3.5 percent readings seen in prior months.

The median forecast, however, tells a slightly different story. While the average declined, the median inflation forecast continued to edge higher, rising from 3.0 percent in February and March to 3.3 percent in April and 3.5 percent in May. Expectations have moderated from April’s spike, but CEOs still see inflation settling at a somewhat higher level than they did earlier in the year.

Corporate Forecasts

The caution is also showing up in CEOs’ forecasts for their own companies:

- 68 percent expect revenues to grow in 2026, vs. 74 percent in April.

- 61 percent anticipate increased profits, vs. 63 percent in April

- 41 percent plan to increase capex this year, vs. 46 percent in April

Hiring is the exception. Forty-six percent of CEOs say they plan to increase headcount this year, up from 44 percent in April. Still, that remains well below the start of the year, when 53 percent expected to increase hiring.

Operating expenses remain elevated: 75 percent of CEOs expect them to increase over the next 12 months, according to the May survey.