For all the talk about disruption and reinvention, most CEOs are still leading companies whose revenue is heavily tied to what they already do, and have done, for a long time.

In a recent Chief Executive survey of 315 U.S. CEOs, 58 percent said less than 10 percent of their company’s current revenue comes from products or services they did not offer five years ago. Only about one in four said at least 20 percent of revenue now comes from newer offerings.

That does not mean CEOs are dismissing innovation. Looking out three to five years, 77 percent said expanding into new categories, markets or offerings will be either critical or important to their company’s ability to grow and remain competitive. Nearly 30 percent called it critical.

The same pattern shows up when CEOs were asked whether their companies had entered new sectors, customer categories, markets or use cases over the past five years. Just 22 percent said those moves now represent a significant source of revenue or growth. A much larger share—43 percent—said they have entered new areas, but those efforts have had limited impact on revenue.

Technologies such as AI are compressing product cycles and opening new use cases. Competitive threats are increasingly coming not only from direct rivals, but from adjacent categories, new business models and companies that redefine the customer problem altogether.

As New Resources Consulting CEO Mark Grosskopf, put it: “AI will have a very large impact much sooner than most expect… all need a plan to address their business model.”

KEEPING UP WITH INVESTMENTS

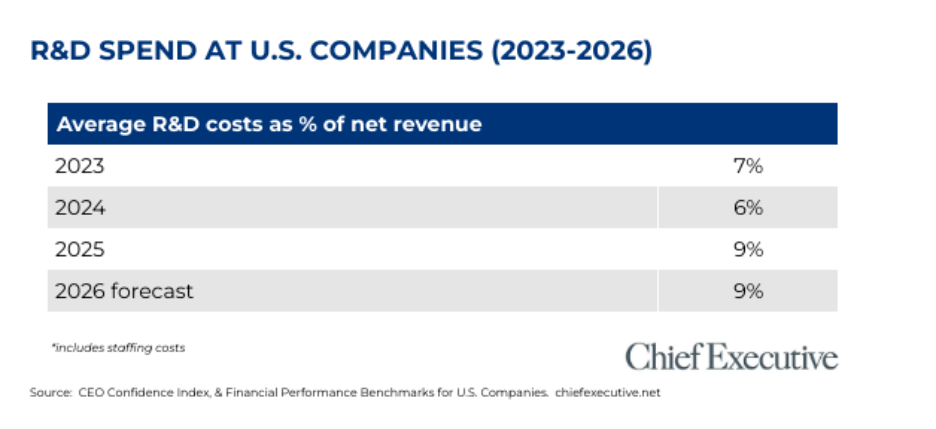

Measured by R&D spending, investment levels vary widely, but the median remains relatively modest.

The survey finds R&D costs at U.S. companies represented an average 8.8 percent of net revenues in 2025, with a forecast of 9.4 percent for 2026. That is up from prior readings of 7 percent in 2023 and 6 percent in 2024, according to our Financial Performance Benchmarks Report for U.S. Companies, but the averages require caution: R&D spending can be skewed by early-stage or technology-oriented companies with lower revenue bases and high development costs. The median response was lower—5 percent for both 2025 and 2026—suggesting that for many companies, formal R&D remains a fairly small share of revenue.

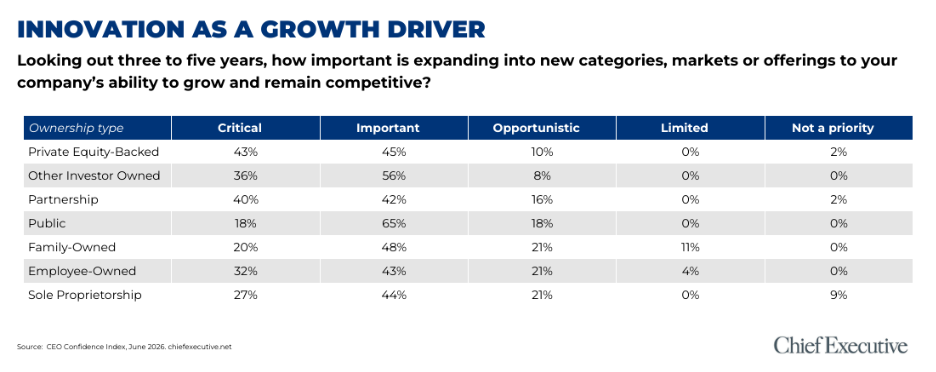

THE OWNERSHIP SPLIT

Ownership type was one of the clearest points of variation in the survey.

Private equity-backed companies were among the most expansion-oriented in our survey. Nearly one-third said new sectors, categories, markets or use cases now represent a significant source of revenue or growth, and 88 percent said expansion into new categories, markets or offerings will be critical or important to future competitiveness.

By comparison, family-owned companies were less likely to report that new areas had become significant revenue sources and were also less likely to rate future expansion as critical or important.

For Taymi Marrero, CEO of manufacturer Ground Power Parts, the contrast is a big concern. “As a small business owner for over 10 years, the biggest challenge I see in the future is big Corps taking over market share and leaving little to no opportunity for growth recovery and expansion for smaller family-owned companies. That is where our country is headed in almost every sector.”

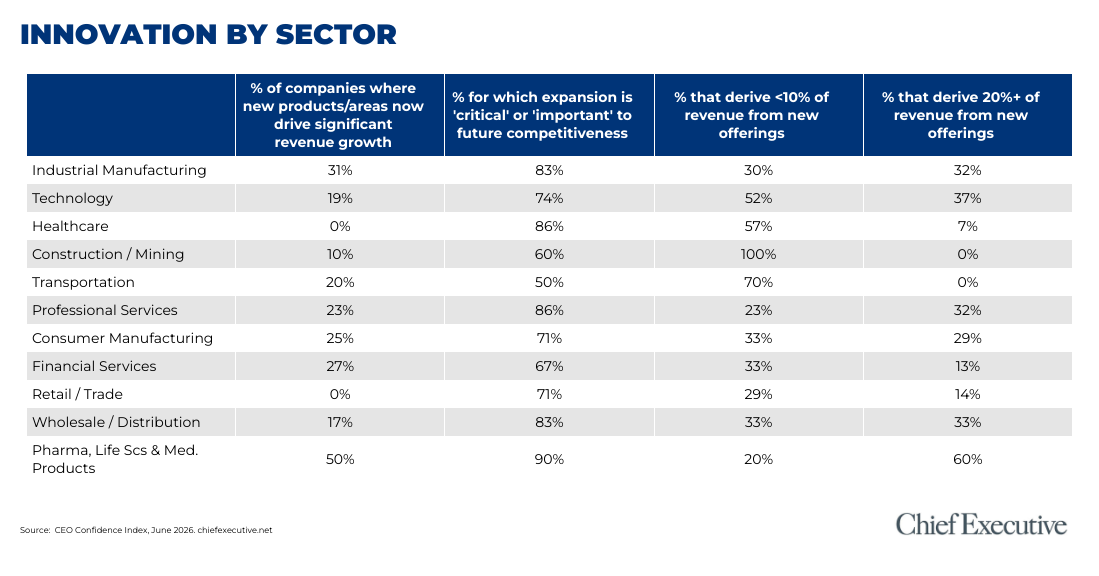

A SECTOR VIEW

Industrial manufacturing, the largest industry group in the survey, stood out on innovation: 31 percent say expansion into new sectors, customer categories, markets or use cases had become a significant source of revenue or growth, compared with 22 percent of CEOs overall. More than eight in ten said expansion into new categories, markets or offerings will be critical or important to competitiveness over the next three to five years.

Technology, software and telecommunications companies also reported high R&D spending as a share of revenue. They were also more likely than the overall group surveyed to say at least 20 percent of revenue has come from offerings introduced in the past five years.

In healthcare, none of the CEOs surveyed said expansion into new sectors, customer categories, markets or use cases had become a significant source of revenue or growth, even though 86 percent said expansion will be critical or important going forward. In construction/mining, CEOs report less than 10 percent of revenue from products or services not offered five years ago.