Innovation is critical to PepsiCo as the consumer-packaged-goods giant tries to separate itself from the irrelevance being suffered by much of Big Food. That is why fully 9% of the company’s

$65 billion in sales now comes from products and brands that are less than five years old, double the percentage of just a few years ago.

To boost that percentage further, PepsiCo has established two corporate venture-capital funds over the last six years, one of them with Unilever. The Pepsi brand has sponsored contests to

solicit the best new ideas from small digital-marketing outfits. And the company has invested quietly in a “health and wellness” startup in Silicon Valley that it refuses to identify.

“Good ‘scientists’ learn to discover things in their own or in others’ labs,” says Mehmoot Khan, PepsiCo’s vice chairman and chief of R&D. “It could be someone else’s recipe that works for you. So give them credit, and recognize them, and also leverage your strengths to make them bigger or better.”

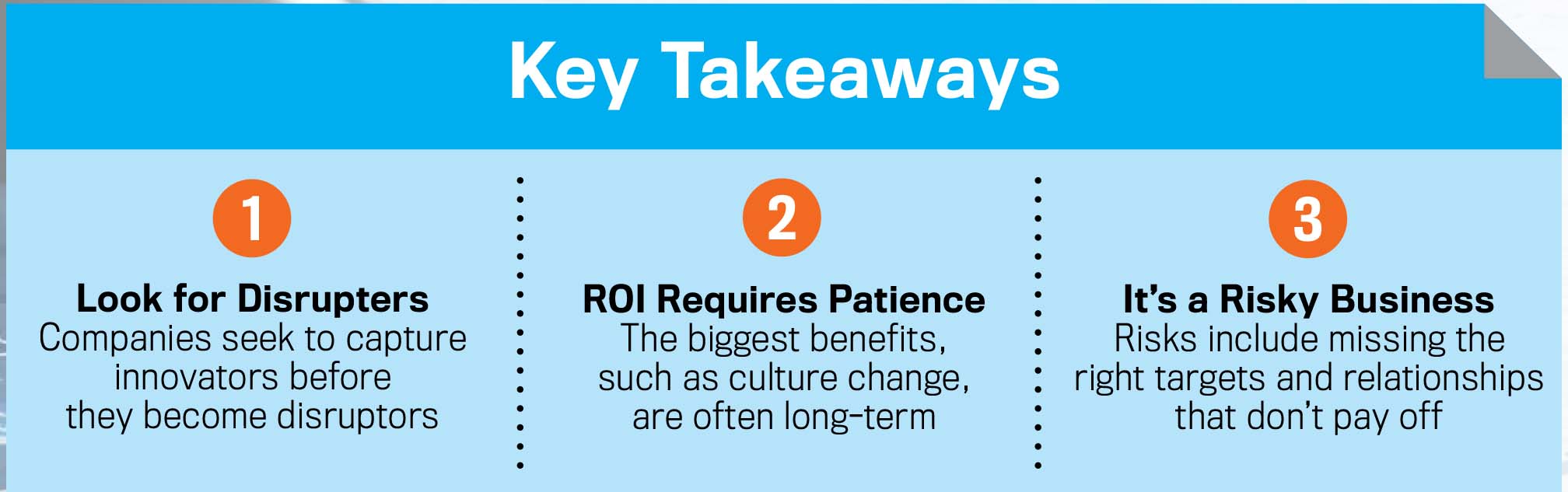

Dozens of other Fortune 1000 and mid-market companies are following similar prescriptions these days as they swallow their provincialism, smash their old business models and avidly seek ties with the really small fry of the universe to get access to innovation and the talent that drives it.

In the hopes of discovering a leap-frogging new product or at least getting a fast pipeline to new ideas and the people who create them, these mid-market and large outfits buy startups, take equity stakes in young companies, initiate and expand corporate venture-capital funds. They rack up partnerships with entrepreneurs, nurture outside enterprises by establishing incubators and accelerators, stage contests, launch vehicles for “intrapreneurial” startups and otherwise plunge into the frothy world of entrepreneurship like never before.

ROILING WATERS

Call it the era of “big-to-small” alliances, an unprecedented explosion of activity that resembles Shark Tank on steroids. This new dynamic subsumes not only the thinking behind the smattering of corporate venture funds that were founded as far back as 20 years ago by Intel and others, but also the aims behind the “open innovation” push established by P&G and a handful of other big companies more than a decade ago.

“There is no doubt about the proliferation of the ‘big-to-small’ mindset especially within the major brands, especially when it comes to the agility and speed in making fast decisions and continuously pivoting yourself as an organization,” says Mayur Gupta, global head of marketing and technology innovation for Kimberly-Clark. In 2014, his company launched an annual

competition at the Consumer Electronics Show in Las Vegas that rewards the winning startup with the opportunity to pilot a project with Kleenex, Huggies or one of the company’s other global

brands. “However, we are not sure if there is any single brand who has figured it out, and in many ways, we are all in the journey right now and at different stages of the course.”

Baron Concors, global chief digital officer for Pizza Hut, notes that “big, iconic brands that aren’t afraid to take some risks” are major participants in the movement—and his division of Yum! Brands is one of them. He takes “regular trips out to California to meet with incubators, and we have done business with a few startups in the last several months,” especially those in digital marketing, Concors said.

“We are constantly in beta mode, always testing and experimenting to see what really clicks, because to really think big you need to start small—and scale up quickly.”

Indeed, one major reason so many companies across the business spectrum (see “Meet the Sharks,” below) have embarked on the big-to-small journey is that they’re trying to answer a common central challenge: how to unlock the secrets to renewed growth when fast-moving small companies and startups seem to hold the keys. The new approach dramatically increases their exposure to startup products, technologies, people and creativity, and drastically telescopes the time, resources and attention required to find and develop worthy new ideas and get them to market.