A decade ago, Frank McDonnell, owner of TurnStyle Brands, a Portland, Oregon-based distributor of premium outdoor scooter products, thought he had a good relationship with his local bank. And why not? Before starting TurnStyle Brands, McDonnell was a banker himself, a portfolio manager for Deutsche Bank. He thought he knew the business.

A decade ago, Frank McDonnell, owner of TurnStyle Brands, a Portland, Oregon-based distributor of premium outdoor scooter products, thought he had a good relationship with his local bank. And why not? Before starting TurnStyle Brands, McDonnell was a banker himself, a portfolio manager for Deutsche Bank. He thought he knew the business.

That was then. After the financial meltdown of 2008, McDonnell’s banker started ducking his calls. Loan applications that used to take weeks now took months; and despite meeting additional documentation requirements, TurnStyle Brands was usually turned down. Applying for an SBA-backed loan was even more frustrating. Then, the CEO got an email from Amazon. If TurnStyle Brands needed credit, the online retailer could help. McDonnell hadn’t even known Amazon was in the commercial-credit business.

It was this former banker’s introduction to an entirely new set of alternatives, non-bank financing for small businesses, all of which can be lumped under the general heading of “marketplace lending” (see sidebar, “What is Marketplace Lending?”). Amazon turned out to have an aggressive lending program, especially for vendors like TurnStyle Brands, which was doing a seven-figure annual business on Amazon. Within 24 hours, TurnStyle Brands had an unsecured $100,000 loan with regular payments over a six-year term at 14 percent interest.

Today, technology, innovation and Big Data are making possible a new, more affordable generation of financial services specifically suited to small- and medium-sized enterprises (SMEs) that remove banks and credit card companies from the transaction. The development comes at a time when SMEs are ill-served by traditional banks.

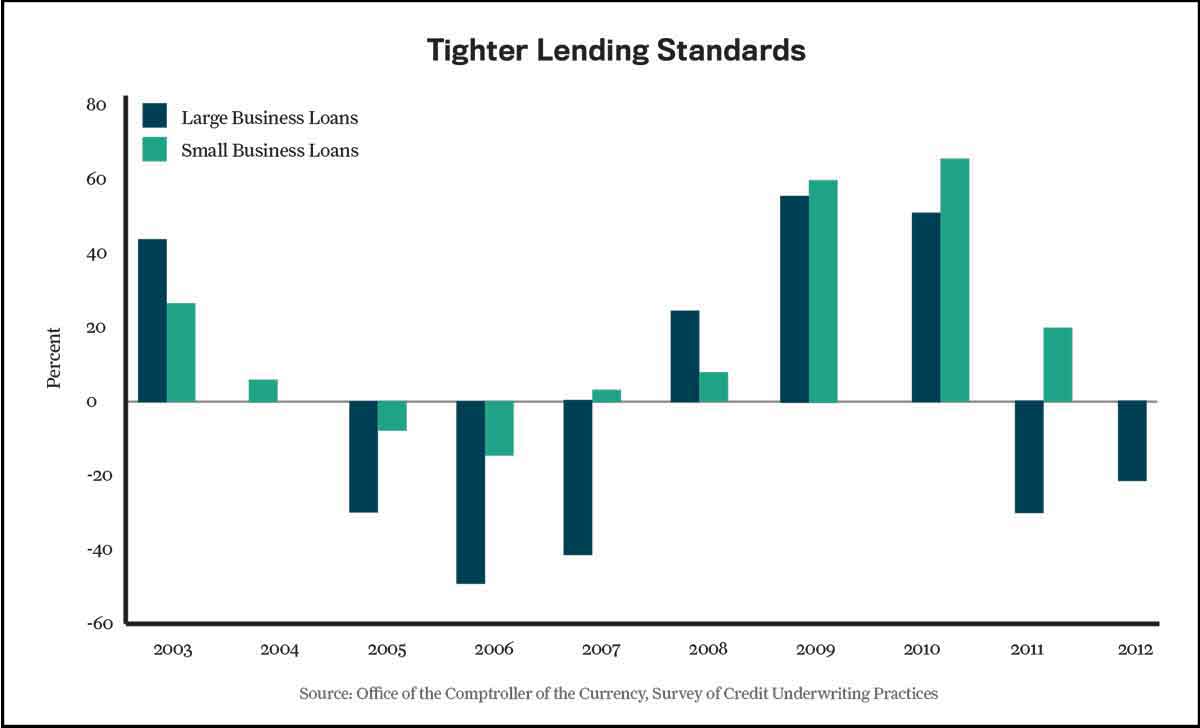

Consider access to capital. Only 39 percent of companies with revenues of less than $5 million succeeded in securing bank loans during the first quarter of 2014, according to the Pepperdine Private Capital Access Index report. In fact, despite a net loosening of credit for big businesses, lending standards for small businesses tightened in 2011 and 2012—a trend expected to continue as banks pursue the largest and most profitable loans. (See sidebar, “Tighter Lending Standards.”)