Exploring Online-Credit Options

Exploring Online-Credit Options

After his Amazon loan experience, McDonnell wondered if there were other, even more affordable, non-bank financial alternatives. A quick search revealed a dazzling array of non-bank online marketplaces for credit-worthy, would-be borrowers.

McDonnell’s research led him to Lending Club, a San Francisco-based company that started off as a peer-to-peer lending site (matching individual lenders with individual borrowers) and transitioned into a company that also finds opportunities for institutional capital.

Five days after filling out a simple online application, he received an approval for $100,000 at 5.9 percent payable over three years. “No tricky math,” McDonnell says. “The interest rate was a third of other financing alternatives that were available to me and it was funded within a week.”

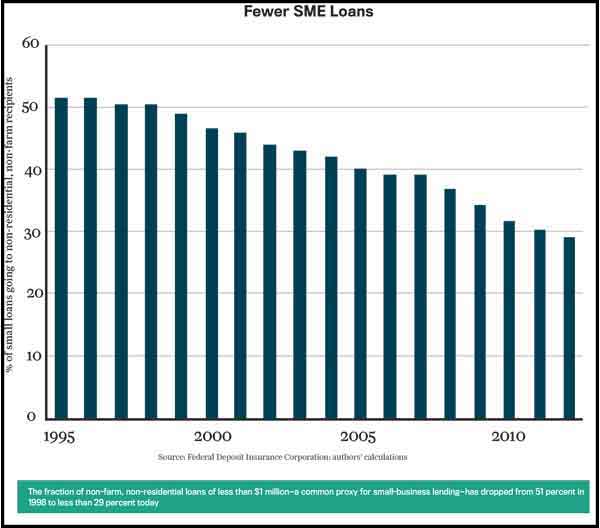

TurnStyle Brands used the infusion of capital to add two new product lines and hire two additional employees. “Small businesses are fed up with banks,” says Charles Moldow, general partner at Foundation Capital in Menlo Park, California. “During the recent economic downturn, when small businesses needed access to credit more than ever, many banks essentially stopped offering loans and called in lines of credit,” he says, adding that two out of every five SMEs saw their credit lines threatened between 2008 and 2012.

Non-bank lending alternatives seek to fill that void. Dozens of credit marketplaces claim to match investors to borrowers who need capital. While interest rates and terms for these alternative-financing options vary widely, competition is clearly lowering lending rates across the board. These third parties are perfecting the business of monetizing liquidity in ways that traditional banks currently cannot touch. Just as web-based sites such as Expedia and iTunes disrupted travel agencies and the music industry, respectively, sites such as Lending Club, Prosper, Dealstruck and many others are allowing SMEs to find the financing they need quickly and on more attractive terms than ever before.

Prior to the introduction of marketplace lending, the alternative-lending industry was a last resort for SMEs, focused on shorter-term loans and higher rates. For example, some merchant cash-advance loans, cash flow loans and revenue loans still demand annual percentage rates (APRs) of over 100 percent or control of a company’s receivables or payments.

However, now alternatives level the playing field. Sites like Fundastic (www.fundastic.com) aggregate information about non-bank loans, many of which feature APRs of 10-20 percent. “Because the loans are funded directly by their investors, the marketplace lenders are able to scale quickly without worrying about the capital reserves on their balance sheets,” explains Yun-Fang Juan, CEO of Fundastic. Marketplace lenders take origination fees from borrowers and investors.

Juan notes that marketplace lending is often the only realistic option if a CEO needs working capital of $25,000 to $100,000. “The reality is that most banks don’t want to bother with loans of less than $25,000 and they want the note to be fully collateralized,” she says. Business owners used to turn to merchant cash advances for this need. Now they have platforms such as Lending Club, Prosper, Funding Circle, Dealstruck and Fundastic offering help, with new sites launched every month.