Debt Crowdlending

Debt Crowdlending

Marketplace lending is essentially crowdlending, or crowdfunding without any equity changing hands. Borrowers pay interest to the investors who they can persuade to fund their loans. For example, Carlsbad, California-based Dealstruck offers SMEs a term-loan product plus a capital line of credit to high-growth startups who don’t meet the credit or size standards of banks. Dealstruck’s team aggregates the borrowers and does all the underwriting. Then, the company invites accredited investors to participate. That’s where the crowd comes in. Investors can either buy into loans on a fractional basis or buy the whole note. Notes average about $100,000, with typical interest rates of 10-20 percent, depending on risk.

Dealstruck takes a first position on assets of the business and also gets a personal guarantee from the CEO. “Our goal is not to disrupt banks, but we fill a liquidity vacuum to enable businesses to access fair, transparent capital to grow healthfully,” says Dealstruck CEO Ethan Senturia.

Dealstruck takes a first position on assets of the business and also gets a personal guarantee from the CEO. “Our goal is not to disrupt banks, but we fill a liquidity vacuum to enable businesses to access fair, transparent capital to grow healthfully,” says Dealstruck CEO Ethan Senturia.

Jake Hansen, CEO of ZTelco, an Internet service provider and telecommunications company in San Diego, looked for financing at a time when massive growth severely strained its accounting system. “We were basically unlendable as far as our bank was concerned because our accounting was in such flux,” says Hansen. The company did, however, have collateral in the form of a data center and number of cell towers.

Hansen submitted an online application to Dealstruck, which inspected ZTelco’s operations and approved a loan of $100,000 at 12 percent within 48 hours. The funds were in ZTelco’s bank account two days later. “The interest rate was very doable, given our profit margins,” says Hansen. “No bank could touch the efficiency of this process.”

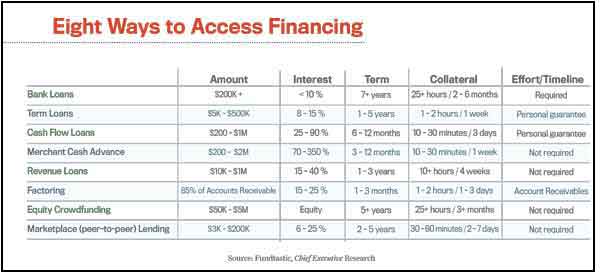

Sidebar: What Is Marketplace Lending?

Sidebar: When Service Companies Need a Loan