In June, the confidence gap between manufacturers’ near-term stressors and their optimism about the year ahead finally appeared to be narrowing. This month, however, that dynamic inverted: Year-ahead sentiment is losing steam, while current confidence holds relatively steady.

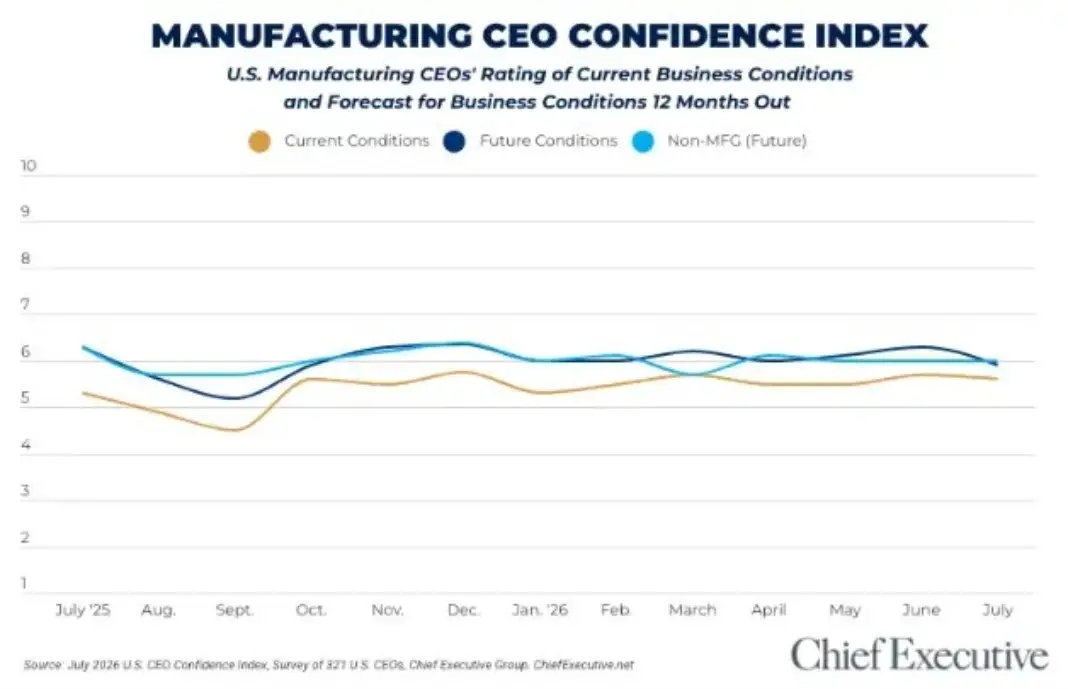

Chief Executive’s latest CEO Confidence Index, fielded July 7-9 among 321 U.S. CEOs, finds manufacturers rate current conditions a 5.6 out of 10, on a scale where 1 is Poor and 10 is Excellent. Though a marginal 2 percent decline since June, this nonetheless remains among the sector’s strongest ratings of the year.

A historical look at current confidence reveals a striking pattern of stability: Ratings have hovered between 5.5 and 5.7 out of 10 since February 2026. Though the sector may have reservations regarding the future, its assessment of the present environment has moved little over the past six months.

When asked about the year ahead, manufacturers forecast business conditions will reach 5.9 out of 10 by this time next year, down 6 percent from June’s more robust 6.3/10. This decline marks the sector’s lowest year-ahead forecast of 2026 and the first time the Index has fallen below 6.0 since October 2025. While that outlook still implies improvement over the current environment, it suggests manufacturers have grown more measured in just how much improvement they expect.

The pullback also erases the optimism gap manufacturers had held over their non-manufacturing peers since May 2026. Manufacturers’ 5.9 forecast now sits just below the 6.0 rating non-manufacturers have afforded for three consecutive months.

Overwhelmingly, manufacturers point to improving, healthy demand as a key factor that buoys current confidence. CEOs simultaneously say, however, that they are concerned about regulatory burden, increasing costs and rapidly shifting policy.

“Revenues are increasing as we see increased demand; however, healthcare, energy and wages have increased. The battle is to improve efficiencies to protect margins,” says Greg Immell, CEO of the small-sized industrial manufacturing firm Saporito Finishing.

John Evans, president of a small-sized lumber manufacturing firm, clarifies the effects of inconsistent policy: “If we can keep the same tariff policies for more than a month, I think the industry will be confident to make plans longer than a few weeks.”

Others agree, citing “higher costs driven by geopolitics [and] interest rates,” painting a picture of strong demand that rising costs are making harder to capitalize on.

ECONOMIC OUTLOOK

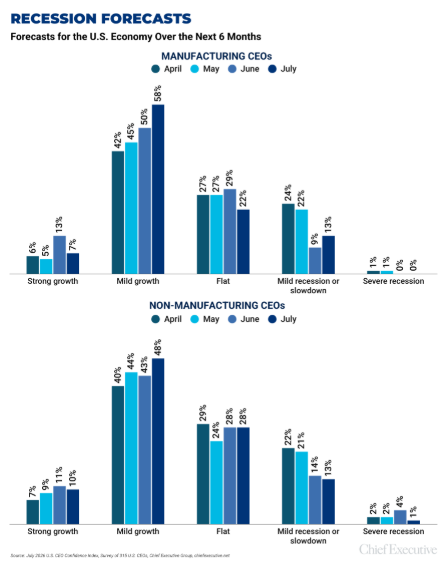

Despite the softer 12-month forecast, manufacturing CEOs’ expectations for the U.S. economy improved yet again in July. 65 percent now forecast some form of growth over the next six months, up from 63 percent in June and the third consecutive monthly improvement. Expectations for growth are centered around more modest additions, with the proportion forecasting significant growth falling nearly 50 percent over last month.

The proportion forecasting some kind of recession ticked up in tandem, from 9 percent in June to 13 percent this month.

Manufacturers yet again fall ahead of their non-manufacturing peers: just 58 percent of the latter forecast economic growth, though their concerns of a recession have softened somewhat (down 22 percent) since June.

DEMAND SHIFTS

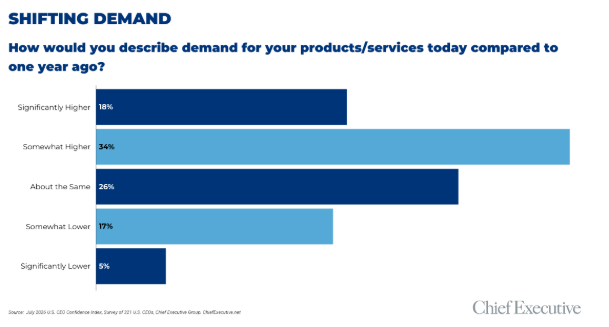

According to those polled, demand continues to underpin the resilience of the manufacturing sector. More than half of manufacturers (52 percent) say demand for their products and services is higher today than it was one year ago, including a notable 18 percent who describe that increase as significant. Just 22 percent say it has declined.

Manufacturers are more bullish on the demand increase than their non-manufacturing peers, among whom just 12 percent describe a significant change.

CORPORATE FORECASTS

Manufacturers’ corporate forecasts were a mixed bag yet again in July:

- 73 percent forecast revenues to increase this year (down from 74 percent in June)

- 67 percent expect profits to increase this year (up from 66 percent last month)

- 37 percent plan to add to their capital expenditures (down from 46 percent in June)

- 42 percent plan to add to their headcount in 2026 (down from 45 percent in June)

A whopping 77 percent foresee increases to their operational expenditures, an increase of 60 percent over June, a month when manufacturers were unusually optimistic about the burden of organizational costs.

About the CEO Confidence Index

Since 2002, Chief Executive Group has been polling hundreds of U.S. CEOs at organizations of all types and sizes, to compile our CEO Confidence Index data. The Index tracks confidence in current and future business environments, based on CEOs’ observations of various economic and business components. For additional information about the Index and prior months data, visit ChiefExecutive.net/category/CEO-Confidence-Index/