That was then. After the financial meltdown of 2008, McDonnell’s banker started ducking his calls. Loan applications that used to take weeks now took months; and despite meeting additional documentation requirements, TurnStyle Brands was usually turned down. Applying for an SBA-backed loan was even more frustrating. Then, the CEO got an email from Amazon. If TurnStyle Brands needed credit, the online retailer could help. McDonnell hadn’t even known Amazon was in the commercial-credit business.

It was this former banker’s introduction to an entirely new set of alternatives, non-bank financing for small businesses, all of which can be lumped under the general heading of “marketplace lending” (see sidebar, “What is Marketplace Lending?”). Amazon turned out to have an aggressive lending program, especially for vendors like TurnStyle Brands, which was doing a seven-figure annual business on Amazon. Within 24 hours, TurnStyle Brands had an unsecured $100,000 loan with regular payments over a six-year term at 14 percent interest.

Today, technology, innovation and Big Data are making possible a new, more affordable generation of financial services specifically suited to small- and medium-sized enterprises (SMEs) that remove banks and credit card companies from the transaction. The development comes at a time when SMEs are ill-served by traditional banks.

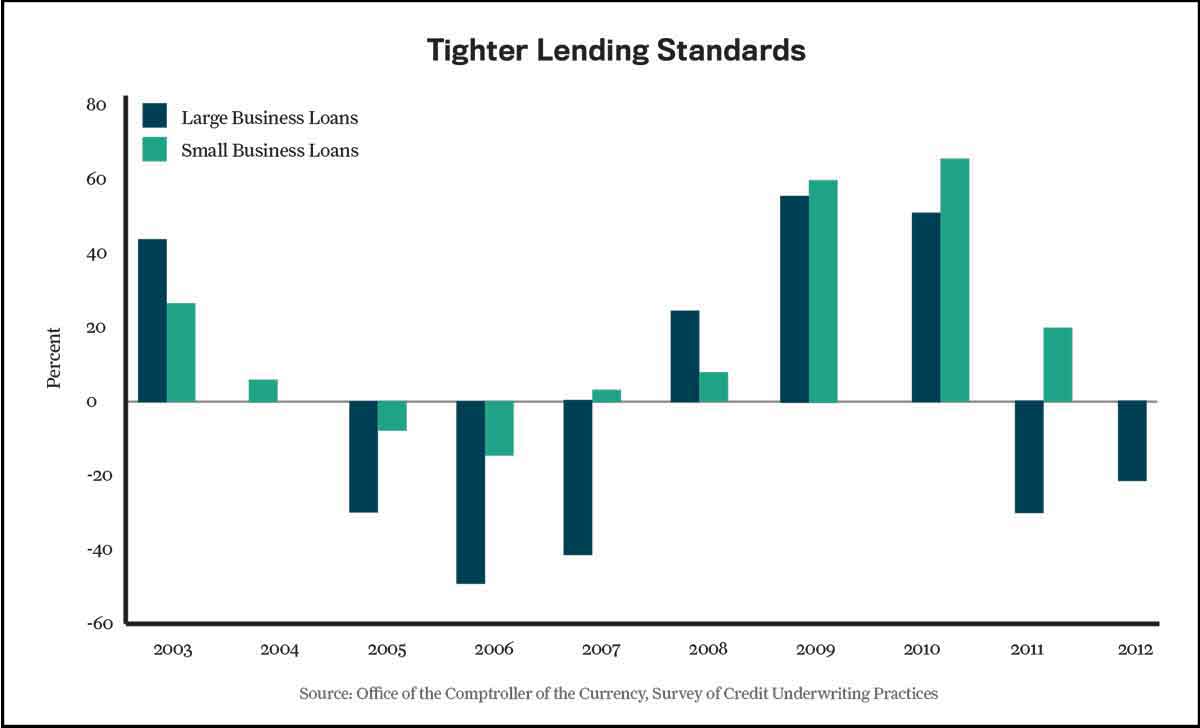

Consider access to capital. Only 39 percent of companies with revenues of less than $5 million succeeded in securing bank loans during the first quarter of 2014, according to the Pepperdine Private Capital Access Index report. In fact, despite a net loosening of credit for big businesses, lending standards for small businesses tightened in 2011 and 2012—a trend expected to continue as banks pursue the largest and most profitable loans. (See sidebar, “Tighter Lending Standards.”)

After his Amazon loan experience, McDonnell wondered if there were other, even more affordable, non-bank financial alternatives. A quick search revealed a dazzling array of non-bank online marketplaces for credit-worthy, would-be borrowers.

McDonnell’s research led him to Lending Club, a San Francisco-based company that started off as a peer-to-peer lending site (matching individual lenders with individual borrowers) and transitioned into a company that also finds opportunities for institutional capital.

Five days after filling out a simple online application, he received an approval for $100,000 at 5.9 percent payable over three years. “No tricky math,” McDonnell says. “The interest rate was a third of other financing alternatives that were available to me and it was funded within a week.”

TurnStyle Brands used the infusion of capital to add two new product lines and hire two additional employees. “Small businesses are fed up with banks,” says Charles Moldow, general partner at Foundation Capital in Menlo Park, California. “During the recent economic downturn, when small businesses needed access to credit more than ever, many banks essentially stopped offering loans and called in lines of credit,” he says, adding that two out of every five SMEs saw their credit lines threatened between 2008 and 2012.

Non-bank lending alternatives seek to fill that void. Dozens of credit marketplaces claim to match investors to borrowers who need capital. While interest rates and terms for these alternative-financing options vary widely, competition is clearly lowering lending rates across the board. These third parties are perfecting the business of monetizing liquidity in ways that traditional banks currently cannot touch. Just as web-based sites such as Expedia and iTunes disrupted travel agencies and the music industry, respectively, sites such as Lending Club, Prosper, Dealstruck and many others are allowing SMEs to find the financing they need quickly and on more attractive terms than ever before.

Prior to the introduction of marketplace lending, the alternative-lending industry was a last resort for SMEs, focused on shorter-term loans and higher rates. For example, some merchant cash-advance loans, cash flow loans and revenue loans still demand annual percentage rates (APRs) of over 100 percent or control of a company’s receivables or payments.

However, now alternatives level the playing field. Sites like Fundastic (www.fundastic.com) aggregate information about non-bank loans, many of which feature APRs of 10-20 percent. “Because the loans are funded directly by their investors, the marketplace lenders are able to scale quickly without worrying about the capital reserves on their balance sheets,” explains Yun-Fang Juan, CEO of Fundastic. Marketplace lenders take origination fees from borrowers and investors.

Juan notes that marketplace lending is often the only realistic option if a CEO needs working capital of $25,000 to $100,000. “The reality is that most banks don’t want to bother with loans of less than $25,000 and they want the note to be fully collateralized,” she says. Business owners used to turn to merchant cash advances for this need. Now they have platforms such as Lending Club, Prosper, Funding Circle, Dealstruck and Fundastic offering help, with new sites launched every month.

Marketplace lending is essentially crowdlending, or crowdfunding without any equity changing hands. Borrowers pay interest to the investors who they can persuade to fund their loans. For example, Carlsbad, California-based Dealstruck offers SMEs a term-loan product plus a capital line of credit to high-growth startups who don’t meet the credit or size standards of banks. Dealstruck’s team aggregates the borrowers and does all the underwriting. Then, the company invites accredited investors to participate. That’s where the crowd comes in. Investors can either buy into loans on a fractional basis or buy the whole note. Notes average about $100,000, with typical interest rates of 10-20 percent, depending on risk.

Jake Hansen, CEO of ZTelco, an Internet service provider and telecommunications company in San Diego, looked for financing at a time when massive growth severely strained its accounting system. “We were basically unlendable as far as our bank was concerned because our accounting was in such flux,” says Hansen. The company did, however, have collateral in the form of a data center and number of cell towers.

Hansen submitted an online application to Dealstruck, which inspected ZTelco’s operations and approved a loan of $100,000 at 12 percent within 48 hours. The funds were in ZTelco’s bank account two days later. “The interest rate was very doable, given our profit margins,” says Hansen. “No bank could touch the efficiency of this process.”

Sidebar: What Is Marketplace Lending?

Sidebar: When Service Companies Need a Loan

AI is reshaping agency talent and forcing leaders to rethink where automation creates value. The…

Strong order books, easing recession concerns and improved access to new markets lifted confidence among…

Winning today takes a combination of AI, technology adaption and trust. A lot of trust.…

‘AI is fundamentally changing how we innovate, and the pace will not wait for us.…

CEO Yellen shares lessons learned from leading a global restoration firm: 'Disasters are unpredictable, but…

2026 has already demonstrated the unpredictability in where, what and how much litigation companies face.…

{kind=link}

{kind=link}

{kind=link}

{kind=link}