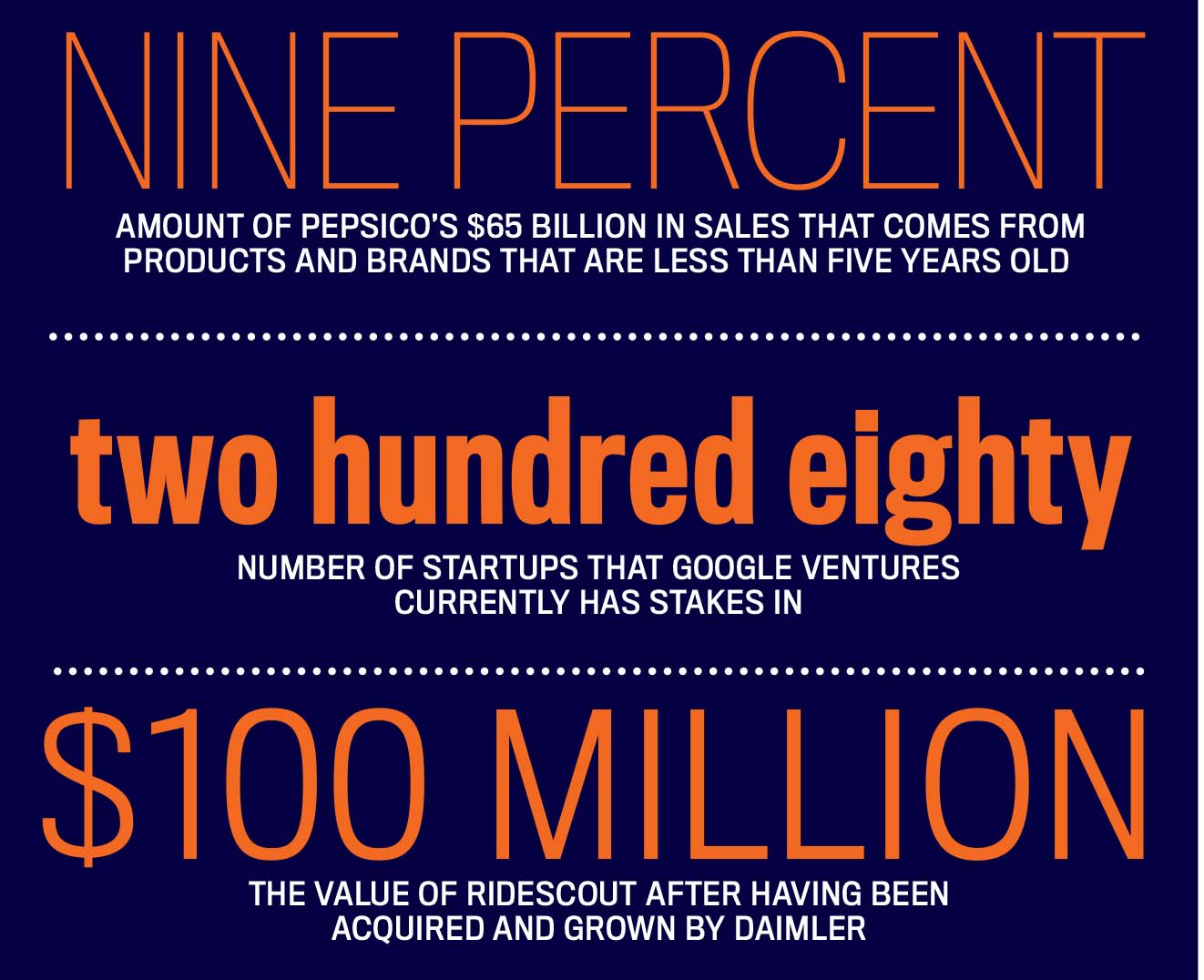

Innovation is critical to PepsiCo as the consumer-packaged-goods giant tries to separate itself from the irrelevance being suffered by much of Big Food. That is why fully 9% of the company’s

$65 billion in sales now comes from products and brands that are less than five years old, double the percentage of just a few years ago.

To boost that percentage further, PepsiCo has established two corporate venture-capital funds over the last six years, one of them with Unilever. The Pepsi brand has sponsored contests to

solicit the best new ideas from small digital-marketing outfits. And the company has invested quietly in a “health and wellness” startup in Silicon Valley that it refuses to identify.

“Good ‘scientists’ learn to discover things in their own or in others’ labs,” says Mehmoot Khan, PepsiCo’s vice chairman and chief of R&D. “It could be someone else’s recipe that works for you. So give them credit, and recognize them, and also leverage your strengths to make them bigger or better.”

Dozens of other Fortune 1000 and mid-market companies are following similar prescriptions these days as they swallow their provincialism, smash their old business models and avidly seek ties with the really small fry of the universe to get access to innovation and the talent that drives it.

In the hopes of discovering a leap-frogging new product or at least getting a fast pipeline to new ideas and the people who create them, these mid-market and large outfits buy startups, take equity stakes in young companies, initiate and expand corporate venture-capital funds. They rack up partnerships with entrepreneurs, nurture outside enterprises by establishing incubators and accelerators, stage contests, launch vehicles for “intrapreneurial” startups and otherwise plunge into the frothy world of entrepreneurship like never before.

ROILING WATERS

Call it the era of “big-to-small” alliances, an unprecedented explosion of activity that resembles Shark Tank on steroids. This new dynamic subsumes not only the thinking behind the smattering of corporate venture funds that were founded as far back as 20 years ago by Intel and others, but also the aims behind the “open innovation” push established by P&G and a handful of other big companies more than a decade ago.

“There is no doubt about the proliferation of the ‘big-to-small’ mindset especially within the major brands, especially when it comes to the agility and speed in making fast decisions and continuously pivoting yourself as an organization,” says Mayur Gupta, global head of marketing and technology innovation for Kimberly-Clark. In 2014, his company launched an annual

competition at the Consumer Electronics Show in Las Vegas that rewards the winning startup with the opportunity to pilot a project with Kleenex, Huggies or one of the company’s other global

brands. “However, we are not sure if there is any single brand who has figured it out, and in many ways, we are all in the journey right now and at different stages of the course.”

Baron Concors, global chief digital officer for Pizza Hut, notes that “big, iconic brands that aren’t afraid to take some risks” are major participants in the movement—and his division of Yum! Brands is one of them. He takes “regular trips out to California to meet with incubators, and we have done business with a few startups in the last several months,” especially those in digital marketing, Concors said.

“We are constantly in beta mode, always testing and experimenting to see what really clicks, because to really think big you need to start small—and scale up quickly.”

Indeed, one major reason so many companies across the business spectrum (see “Meet the Sharks,” below) have embarked on the big-to-small journey is that they’re trying to answer a common central challenge: how to unlock the secrets to renewed growth when fast-moving small companies and startups seem to hold the keys. The new approach dramatically increases their exposure to startup products, technologies, people and creativity, and drastically telescopes the time, resources and attention required to find and develop worthy new ideas and get them to market.

Also, CEOs want to inoculate their companies against fast-moving hornets, if possible, before being stung by them. They recognize that, in many industries, new and nimble smaller companies have been strapping up the Gulliver-like major players like never before; think of Uber and auto makers, or Sparkling Ice waters and soft-drink brands.

“More incumbent companies are worried about disruption than ever before,” says Tom Ciccolella, U.S. venture-capital leader for PwC, the consulting firm. “Or they want to make sure they have the finger on the pulse of what might be disruptive to their business.”

These companies searching for investments specifically see that startups tend to have a better grasp on the digital technologies that have become crucial to nearly all industries and usually possess a better understanding of the sensibilities of the key millennial generation—in large part because many of the entrepreneurs themselves are members of it.

Savvy chiefs of large and mid-size companies also want to get access to the best talent, and direct relationships with entrepreneurs are one of the best ways. And advocates of a big-to-small strategy see value in the possibilities for revitalizing their own ossified company cultures in the process.

“The real [key performance indicator] is—have we fundamentally changed how people think and how we’re preparing to enter into the next generation of our approach to organization?” says Bonin Bough, vice president of global media and consumer engagement for snack giant Mondelez International, which has launched accelerators for startups in both mobile tech and shopper marketing. “We have recognized that we can bring a startup mentality and culture shift into the organization.”

On the flip side, startups are greeting this development with open arms. Many indeed have the stuff that big companies are seeking, but the little guys usually lack the resources and backing to prove, market and scale their innovations.

Larger-company sponsorship can provide exposure, clients, capital, distribution, sales growth, marketing muscle, financial expertise and other things of commercial value—and, of course, maybe the ticket for them to reach the next level of business or strike it big.

“We could have built [a streaming platform] ourselves, taken a year and a decent amount of money,” says Hilary Perchard, head of U.S. investments for Sky. “But instead we searched and found Roku in Silicon Valley. We’ve also used their technology platform to grow Now TV and our overall business at a faster rate than in 10 years thanks to the rate at which it engaged consumers.

“For Roku, it has given them the huge success of distribution in a market where they didn’t have that much traction before. So it has proved to be hugely synergistic for both them and us. And since then, they’ve been cutting similar deals with operators around the world.”

Similarly, KPMG in 2013 created KPMG Capital as a fund “to invest in the best and brightest data-analytics technologies that we can take to our clients,” says Mark Toon, CEO of KPMG Capital. Its first investment was in Bottlenose, a $20-million, Los Angeles-based “trend-intelligence” company.

“We’re not the most innovative organization in the world when it comes to creating new technologies to do stuff that’s cutting-edge,” he says of KPMG, the New York based global accounting and consulting firm. “Our investment in Bottlenose was our way of ensuring that we can provide our clients with the brightest thinking in a specific space that we wouldn’t get to for years, if ever.”

Two years ago, Molex, a Lisle, Illinois-based major maker of electronic components, formalized a program of investments in “external innovations that can specifically disrupt our future vision, or in strategic growth areas to get us a jump start in new technologies,” explained Lily Yeung, director of corporate development for the company that Koch Industries acquired in 2013.

Last year, Molex invested in a round of convertible notes and struck a strategic partnership agreement with NuCurrent, a Chicago-based wireless-antenna design outfit. That followed by a year Molex’s similar investment in Vasa Applied Technologies, a startup that developed a technology for accurate measurement of fluid flow rates for medical applications.

For Vasa, says co-founder and CEO Jacob Polger, the opportunity is clear. “With Molex’s global sales force and engineering capabilities, we expect to significantly increase our technology

reach in new geographies and markets,” he says. For Molex, the deals are a way to place more bets on the future.

“It’s related to the many unicorns we see in the startup world,” Yeung says, referring to the term for a new company that quickly burgeons into a big one. “Big companies are learning that these small companies can disrupt their core businesses and become really valuable as well, and tapping into innovation is absolutely crucial for our survival.”

THE MIDDLE MINDSET

Savvy mid-market companies are participating in this trend as well. Executives of Kwikset, for example, a $600-million maker of residential locks owned by Spectrum Brands, in 2012 saw a startup called UniKey on Shark Tank demonstrate a digital “smart lock” that threatened the traditional security devices where Kwikset reigned.

The company quickly partnered with UniKey to introduce its own smart lock ahead of its rivals. The relationship also is making all of Kwikset more nimble. “We looked at our own organization internally and decided to evolve our structure to be more like a small company,” explains Greg Williamson, Kwikset’s chief marketing officer.

“In some ways, mid-market companies are better positioned than big companies for this, because they still possess a fairly nimble structure, making the interface with startups less of a disconnect,” notes Mike Morin, COO at Start Garden, a venture-capital fund based in Grand Rapids, Michigan. “They often have significant regional social capital and relationships through

their employees and their supply base, and that makes them a more likely access point for local innovators.”

While it’s almost too early to recognize failures, a big-to-small strategy clearly carries some risks for both sides. For big companies, the method remains essentially a crapshoot, providing little of the traditional ROI metrics that they typically have used to make investments. And they still may not avoid disruption by some startup that they passed over.

For small companies, the risks are big as well. They may select the wrong big partner and then not be able to escape a corporate vice grip that is fortified by lawyering, or they may be suffocated by their corporate relationships instead of transforming their much larger partners.

But big-to-small thinking is already blowing a big hole in traditional business models and relationships. And it seems here to stay.

Here is a partial roster of major companies taking a big-to-small approach that aren’t covered in the main story.

CHOBANI has launched a food incubator in New York City, selecting about 10 companies to provide with test kitchens, office space, mentorship and access to chefs and other Chobani resources, with an initial $2 million investment.

DAIMLER acquired RideScout as the platform for an urban-mobility play and already has developed it into a $100 million business.

DIAGEO launched Diageo Technology Ventures to partner with innovative digital and technology companies to the tune of $100,000 each and started Distill Ventures, which is investing up to $15 million in supporting and nurturing startups and new ideas ranging from vermouth to gin, in Western Europe and beyond.

FORD is teaming with suppliers Verizon Telematics and Magna International to fund an incubator that will support transportation-related startups, investing $2 million in Techstars Mobility, driven by Detroit to help 30 companies get off the ground in the next three years.

GOOGLE through its Google Ventures arm has close to $2 billion in assets under management with stakes in more than 280 startups. They include hundreds of millions of dollars alone invested

in one research startup, Calico, whose ultimate goal is to help human beings live hundreds of years.

KROGER AND TESCO backed a joint venture called Dunnhumby Ventures, which is looking for innovations and making investments in startups seeking to transform the future of retail.

NIKE has been a pioneer with programs such as the Nike+ Accelerator to drum up new ideas for its fitness devices, and the Launch Systems Innovation Challenge, aimed at garnering innovative ideas and processes to transform the way fabrics are made.

WALT DISNEY has a small business accelerator.

Exelon: Prizing Entrepreneurship

Few industries would qualify as more old-line and conventional than the Rust Belt electric-utility business. But Chicago-based Exelon has emerged from that with a pace-setting big-to-small strategy that belies its traditional roots.

Last year, for example, Exelon invested in two local startups “that have had a real impact for us,” Sonny Garg, the company’s chief information and innovation officer said in 2014. ADMCi is a “design thinking” school, and the other new Exelon partner, AKTA, is a mobile-development company that since has been recognized as an Inc. 500 company.

“We’re looking to drive a culture of innovation, develop emerging technologies and work with entrepreneurs,” explains Brian Hoff, Exelon’s director of emerging technology. “We’ve even shown the board our program. From a high-level program with board-level visibility, down into the weeds with specific startups—everything weaves together.”

One successful “weed patch” for Exelon has been an annual program it began in 2013 called “Dancing with Startups,” in which the company hosts emerging startups at a smattering of cities across the country for a day of presentations and partnership discussions. It offers prize money for the best ideas and business models, and it has brought some of the entrepreneurs into the company “to try out their products and technologies,” Hoff says.

Hoff notes that the process already has produced a steady deal flow. Exelon’s courting of outside innovators also has raised the company’s esteem in the eyes of its own employees, based on

internal questionnaires, and is “impacting the culture,” he says.

Of course, there are dangers for the company in plunging so dramatically into the exciting new realm of the startup: Garg recently resigned to join one of the startups in which Exelon invested, Uptake, a data-analytics company.

Everspin chief Aggarwal discusses long-term supply commitments, engineering for durability and the leadership decisions required…

C-Suite leaders who insist on rigorous and routine examination of their AI processes are the…

The CEO of global accounting software company Xero knows if she can understand a plan’s…

Handled well, a leadership transition is less a single announcement than a series of deliberate,…

Market engineering is far more than clever marketing. It’s the operating system for category ownership…

Aprio CEO Richard Kopelman on 14 deals in a year, a $300 million AI bet…

{kind=link}

{kind=link}

{kind=link}

{kind=link}