Other academics draw the same conclusion. Their research indicates that holding back has its virtues. “There is much more evidence to suggest that it is better to be second than first,” says Aleksios Gotsopoulos, Ph.D., assistant professor of management at Sungkyunkwan University in South Korea. “Once a market has been proven, a fast follower with capital, distribution channels and innovative marketing can come in with a superior product, satisfying customer needs that the early mover had failed to satisfy. Being first does not mean winning.”

FIRST TO WIN, FIRST TO LOSE

He makes a compelling point. Southwest wasn’t the first airline, but it is the preeminent air carrier today. Google wasn’t the first Internet search engine, Kickstarter wasn’t the first crowdfunding site and Boeing wasn’t the first airplane manufacturer. In fact, the latter company shrewdly analyzes whether it is better to be first-to-market with a new airplane or be second

with something better. (Fair disclosure: The reporter is the author of the book Higher: 100 Years of Boeing.)

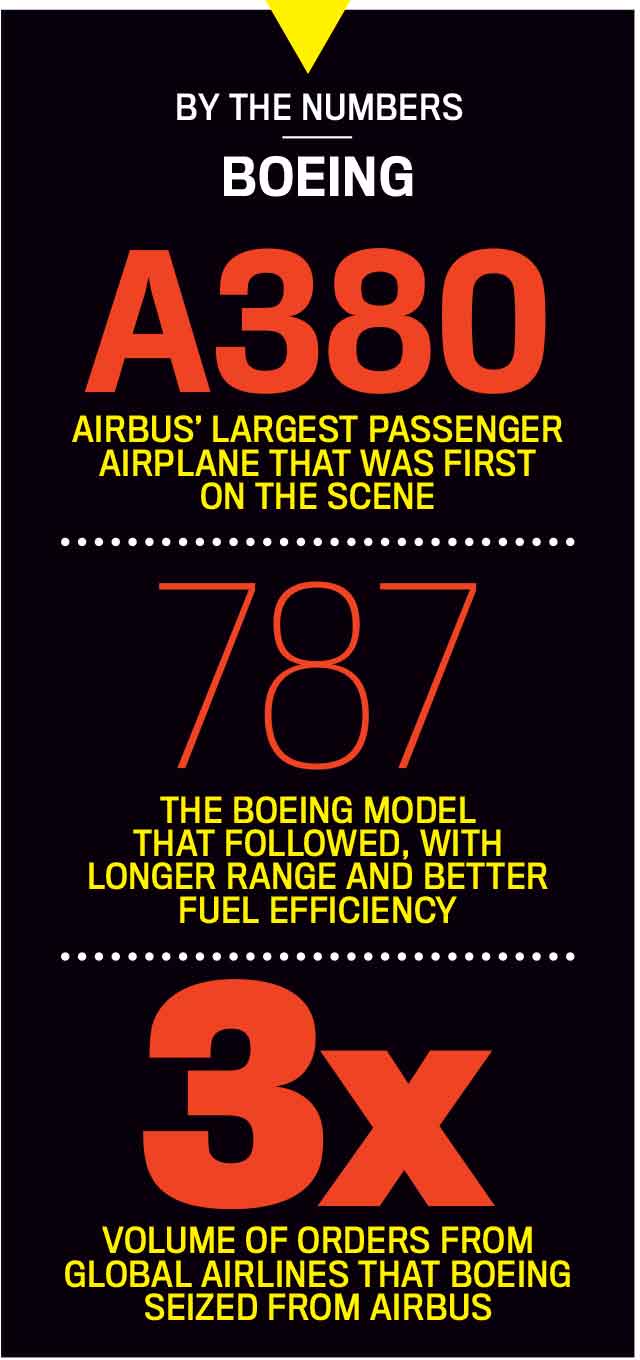

Boeing’s 787 Dreamliner demonstrates the wisdom of waiting. Prior to the Great Recession, airlines wanted next-generation aircraft with higher passenger capacity for hub-to-hub routes. Boeing’s chief rival Airbus responded first with plans to build the A380, the world’s largest passenger airline. Boeing instead planned to develop a supersonic jet. When the financial crisis reared, Airbus stuck to its plans but Boeing went in a completely different direction, developing the smaller capacity, but longer-range and more fuel-efficient 787. The company figured that

during the difficult economic period, airlines would want more efficient planes with lower operating costs.

Airbus hit the market first, but Boeing had the more appealing product. Even though the Dreamliner’s debut was postponed because of supply chain issues, it seized more than three times the volume of orders from global airlines than the mammoth A380. By taking its time, Boeing could assess Airbus’ market experience and deliver a product better suiting demand. Both manufacturers had great products, but in this case the early bird did not get the worm. This is not to conclude that all early movers run the risk of a bad fate or that the real advantage belongs only to those that follow. First movers can neatly tie up patents and copyrights, cultivate strong alliances with regulators, and build unshakable brand loyalties.

Shenkar says being first-to-market or second-to-market is less important than having excellent market timing. Nevertheless, he insists that it is generally better to follow than to lead. “There is no reason to rush to market, even though analysts continually tout it as the surest way to gain and hold market share,” he explains. “While the innovator enjoys some preliminary

advantage, the return on this innovation goes down over time.”

Many first movers make the mistake of jumping in too soon with an ingenious product, hoping to create a market sensation. In such cases, it is not uncommon for the innovator to give less thought to the supply chain, order fulfillment, distribution channels, regulatory compliance and back-office finance and accounting aspects of profiting on the product. Having spent a bundle on R&D and production, they may be short on capital to make quick adjustments correcting mistakes. The fast follower has these elements in place and can quickly pounce with an improved alternative that may also be less expensive.

There is value in letting the early movers absorb the first blunders. This wisdom helped the launch of crowdfunding marketplace CircleUp, an online intermediary between private equity investors and startup companies. CircleUp deliberately waited to see how earlier equity-based crowdfunding sites fared before it opened its virtual doors in 2012. “The first movers wanted to be all things to all investors,” says Ryan Caldbeck, CircleUp founder and CEO. “There would be tens of thousands of startups looking for investments, with most of them just dying on the

platform because the investors were confused and frustrated.”

Caldbeck had a better idea. “We decided to focus on startups in one industry—consumer products and retail—and reach out to investors that were solely private equity,” he explains. “We also curate the ventures that reach out to us, eliminating 98 percent of applicants. This way, the right ideas reach the right investors.” He adds, “This is not about first-to-market, it’s about first-to-market fit.” The strategy is working. CircleUp has expanded the number of startup companies it works with by 10 times since July 2013.

DARE TO REDEFINE

Other late entries win market share from early movers by redefining a category, which was the case with Burlington, Vermont-based Sustain Condoms. Like Starbucks, by no

stretch the world’s first coffee shop, Sustain came to a mature market with a new product and novel marketing message. “Our goal is to get people to think about sustainability and corporate responsibility every time they open a condom package, even though they’re understandably distracted,” says Jeffrey Hollender, the company’s founder and CEO.

Sustain’s condoms are made from natural latex, the sap of the rubber tree, a renewable, sustainable material unlike synthetic rubbers. The packaging is recyclable and Sustain gives 10 percent of profits to support women’s reproductive healthcare. The company is leveraging these brand equities with a unique target market—women. “Forty percent of condom purchasers are women, but the product is aimed at men,” Hollender says. “We wanted to make a product that was aimed and owned by women. We sincerely hope this will increase condom use by single, sexually-active women, which is 19 percent.”

The condom’s packaging is in a Tiffany-like blue-green color, with pictures of shells and wet rocks. Advertising is confined primarily to women’s health and beauty magazines like Self. Launching in 2014, the product is now available online and in more than 1,000 stores nationwide.

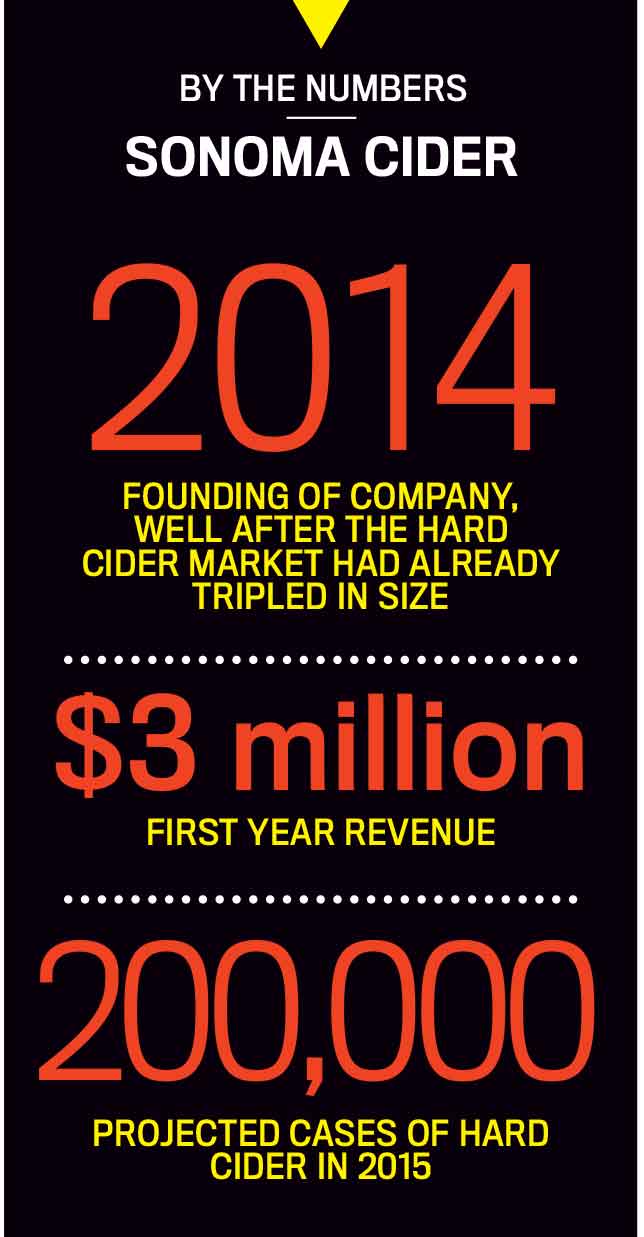

Another fast follower that is redefining a category is Sonoma Cider. Longtime beverage industry executive David Cordtz saw that hard cider sales were beginning to rise in the mid-2000s. In the 1970s, Cordtz was the youngest commercial wine maker in California’s Napa Valley with Cordtz Brothers Cellars. He sold the winery in the early 1980s, but stayed in the industry in a variety of sales and production positions, dreaming about running his own company again.

Cordtz entered the fray with a product that took the category in a new direction—hard cider made from organic heirloom apples and pears harvested in Washington State’s Yakima Valley. “They taste better and are vegan and gluten-free,” he says.

He marketed his cider blends, Hatchet, Anvil and Pitchfork, to health-conscious Millennials and Gen X-ers at youth-oriented music festivals like Coachella. The effort paid off. Organic hard cider has caught on with Millennials in the same way that craft beer caught on with their parents. Sonoma Cider is now sold in 24 states, producing more than 70,000 cases and chalking up an impressive $3 million in revenue in its first year of business. The company is on track to produce 200,000 cases in 2015.

BETTER FAST FOOD

Even in deeply entrenched markets like fast food, followers can beat the early movers by giving consumers more choices, better food and more upscale dining environments. Two fast casual—and fast-growing—restaurant chains taking this route are Boloco and Paxti’s Pizza.

Boston-based Boloco sells burritos in an upscale environment, taking its cue from pioneer Chipotle Mexican Grill. Where it differs is in the variety of its fare. “We’ve got more than a dozen

different burritos on the menu besides Mexican,” says Patrick Renna, co-founder and CEO of the chain of 20 restaurants throughout the Northeast. “This way a diner can come here on multiple

occasions, even in a single week, and find something different. They don’t get tired of eating Mexican all the time.”

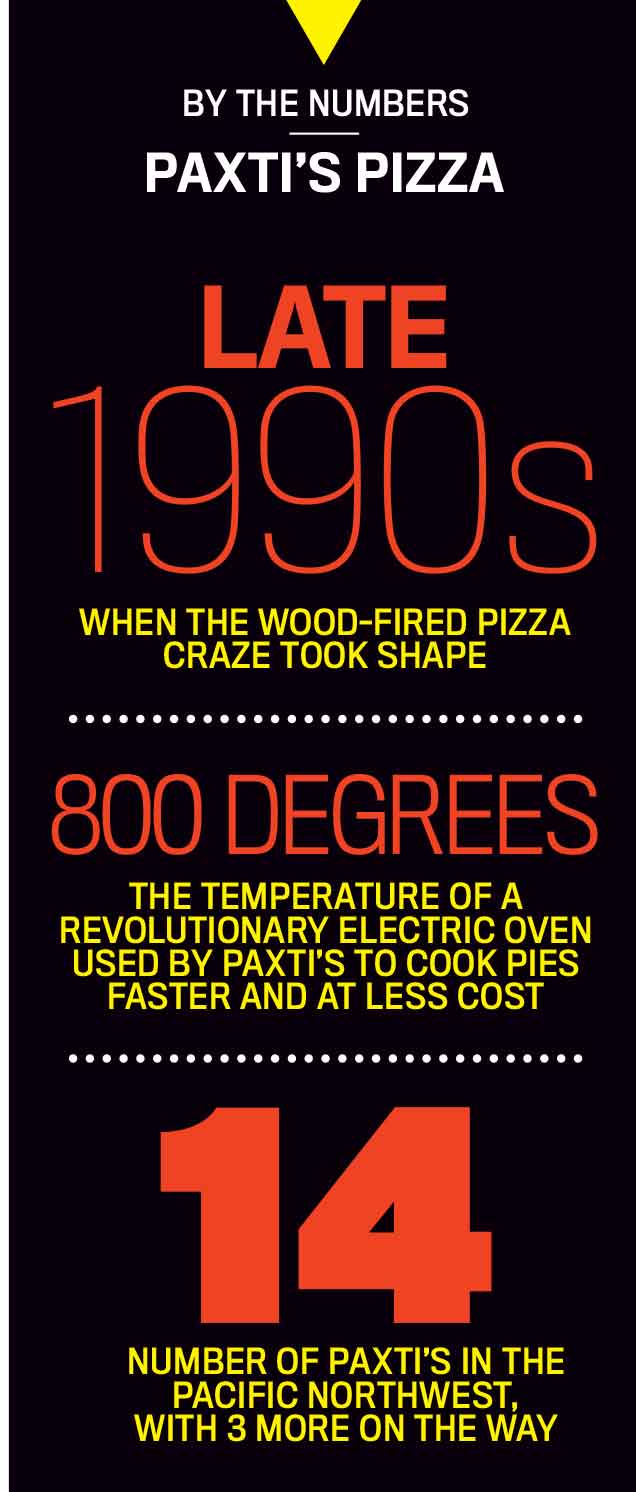

At San Francisco-based Paxti’s Pizza, founder and CEO Bill Freeman, who had launched several successful Silicon Valley technology startups like United Telecom, watched from the sidelines as the wood-fired pizza craze took shape in the late-1990s and early 2000s. Pizza chain pioneers like Pizza Hut and Domino’s, despite much cheaper prices, were fast losing market share to startups like Seattle’s Tutta Bella, which baked its pies with better ingredients in ovens fed by burning wood, which cook crispier crusts. “Next thing you knew, every town across America had a small pizza chain with wood-fired ovens,” Freeman says.

With money not a problem and lots of time on his hands, the successful entrepreneur was eager to enter the market with a childhood friend, Francisco “Paxti” Aspiroz. The latter had heard about a revolutionary electric oven manufactured in Italy that quickly reached a temperature of 800 degrees, much hotter than a wood-fired oven. It also cost less to operate than both gas-fired and wood-burning ovens, and delivered cooked pies in 30 percent less time. “Our motto is ‘better before cheaper, and revenue before cost,’” Freeman says.

The founders launched Paxti’s Pizza in 2004 in Berkeley, California. It didn’t hurt that the original office of Facebook was next door or that its founder Mark Zuckerberg survived on its pies (smudged boxes bearing the company’s name can be seen in the movie The Social Network). Today, there are 14 Paxti’s restaurants in the Pacific Northwest, and three more under construction.

In both cases, innovative latecomers like Boloco and Paxti’s were able to take advantage of the pioneering brands’ perceived shortcomings. “The innovator does most of the work, invests the greatest amount in R&D, prepares the market and makes the most mistakes,” says Shenkar. “For this they get the early returns. But, unless they maintain continuous innovation and continually lower costs, someone is sure to come in, copy what you do best and innovate the rest.”

WILL PATIENCE REWARD?

Fast followers will not make a dent in or dominate a market unless they have resources, infrastructure and relationships. Freeman had the money, expertise and agility to hit the ground running. So did Hollender, who possessed distribution savvy and sharp marketing skills. In another mature market—household products—in 1988, he founded Seventh Generation, which makes products from biodegradable plant-based materials. With Sustain, he is simply leveraging the same message of sustainability and natural resource conservation, not to mention

many of the same retail channels.

Cordtz also had strong ties to distributors, in his case with hundreds of taverns and restaurants across the country, thanks to his previous job as national sales manager for Thames America, a British maker of hard cider. He had similar contacts in liquor stores and other establishments selling wine and beer. He also had the inside savvy to buy state-of-the-art fermenting equipment from a manufacturer in China he knew, at a discount. The machines were reengineered using sensors and data analytics to reduce labor costs.

“It would be a stretch to say we had a second-to-market strategy,” Cordtz says. “Hard cider was once the largest alcoholic beverage category in America, a position that lasted until Prohibition. We’re just coming at the market with something different.”

He has a point. In many ways, fast followers aren’t reinventing the wheel. They’re simply making better products to customers’ tastes, whether it’s airplanes, pizza or condoms. First acts get the audience going. Second acts get the applause.

Despite research indicating that many first-to-market companies incur steep declines in customer demand, not all early movers suffer this dismal fate. To capture market share and retain this

leading position, early movers must continually innovate.

“Once you set your technology as the industry standard, you must make it increasingly difficult for followers to catch up,” says Sungkyunkwan University’s Gotsopoulos. “You do that by making your product or service increasingly more responsive to customer needs.”

BlackLine, the market-leading provider of integrated financial close automation technology, fits this profile. Launched in 2001 with a handful of employees to automate a single client’s account reconciliation process, the company was the pioneer in the soon-to-burgeon financial automation market.

Today, it serves more than 950 clients, from major enterprise-level companies through the mid-market tier, and tallies over 300 employees.

In between is a story of listening to client complaints about their other time-consuming, manual processes to close the books, and then acting upon this information. “We’re in a constant mode of asking ‘What do you need, what can we do better?’” says Therese Tucker, BlackLine founder and CEO. “Much of our functionality derives from customers expressing an issue and us working on ways to fix it.”

For instance, when corporate accountants grumbled about having to manually file journal entries, BlackLine developed an automated solution taking the drudgery out of the process. When they carped about having to manually reconcile and settle intercompany transactions, and manually identify deviations in the balance sheet and P&L statement, two additional functions were added to BlackLine’s growing platform. The technology simply kept getting better, innovation after innovation. Accountants were liberated to focus on value-added tasks, their CFOs acquired enhanced visibility into business data, and controllers gained more control over reporting and compliance.

Not only has BlackLine been able to maintain its market lead over second-to-market competitors like Trintech, but its growing solutions platform also encouraged Gartner to create an entirely

new category of financial technology—Enhanced Finance Controls and Automation. “We’ve learned that to stay on top, you have to be more creative than your competitors,” Tucker says. Or as Gotsopoulos puts it, “Never leave room for seconds.”

Featured image property of iStockPhoto.

How the firms separating from the pack are turning AI from an IT line item…

In the volatile swirl of 2026, so many companies are having a tough time accomplishing…

Everspin chief Aggarwal discusses long-term supply commitments, engineering for durability and the leadership decisions required…

C-Suite leaders who insist on rigorous and routine examination of their AI processes are the…

The CEO of global accounting software company Xero knows if she can understand a plan’s…

Handled well, a leadership transition is less a single announcement than a series of deliberate,…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}